Alipay vs PayPal: A Comprehensive Comparative Analysis for Global Digital Payments

Introduction

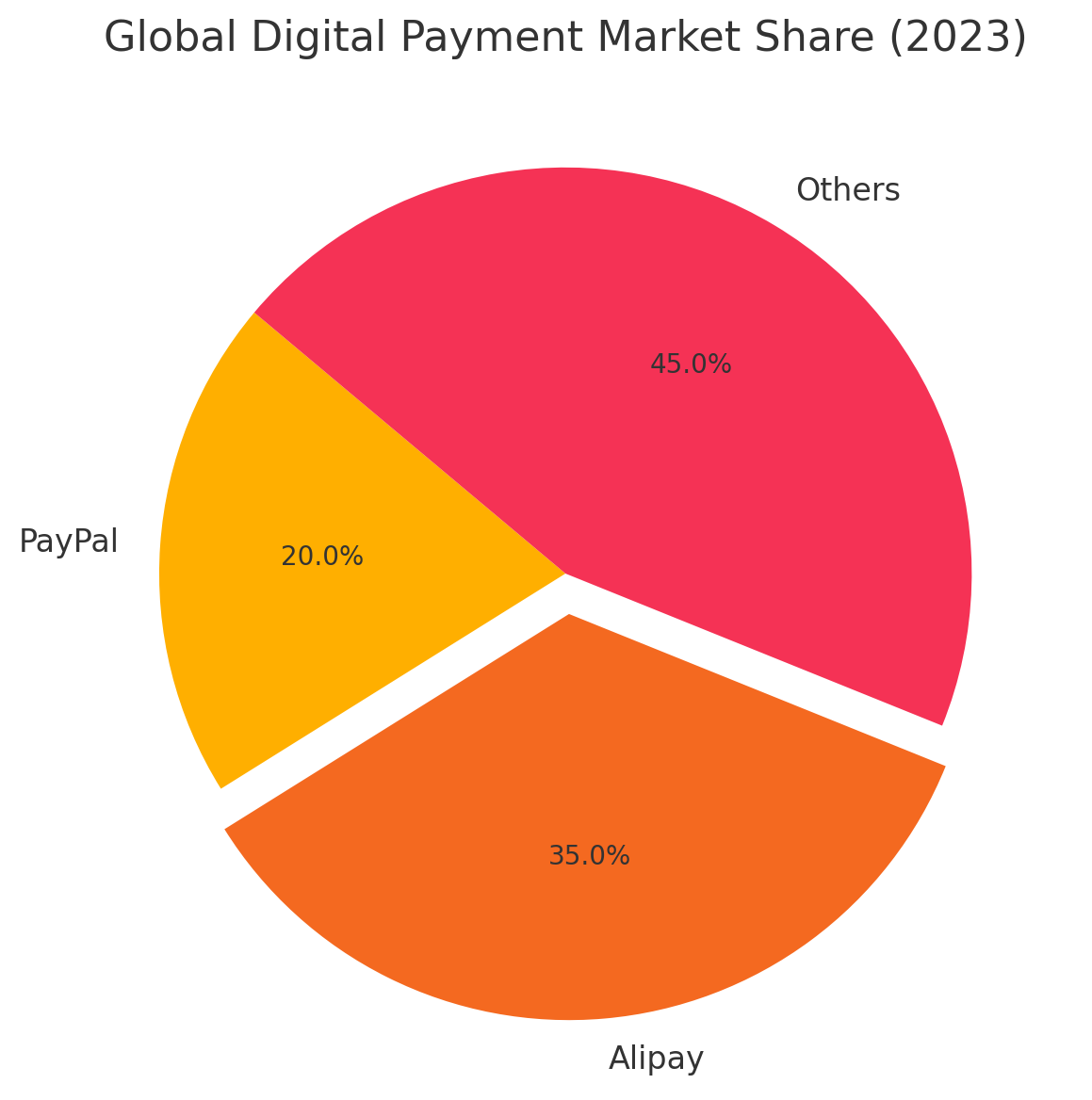

The world economy is undergoing a dramatic shift from traditional cash-based transactions to digital payment systems. Among the leading players shaping this transformation are Alipay and PayPal, two fintech giants that dominate their respective spheres of influence. While PayPal has been a pioneer in online payment solutions in the Western world, Alipay has revolutionized financial transactions in Asia, particularly China. This post explores the Alipay vs PayPal debate, analyzing their history, business models, security features, regulatory challenges, customer experience, and future prospects in a rapidly digitizing global economy.

The comparison between Alipay and PayPal highlights not only the technological and economic competition between East and West but also the diverging philosophies of fintech innovation—PayPal as a global payment facilitator and Alipay as an ecosystem-driven financial super-app.

Historical Background

Origin and Evolution of PayPal

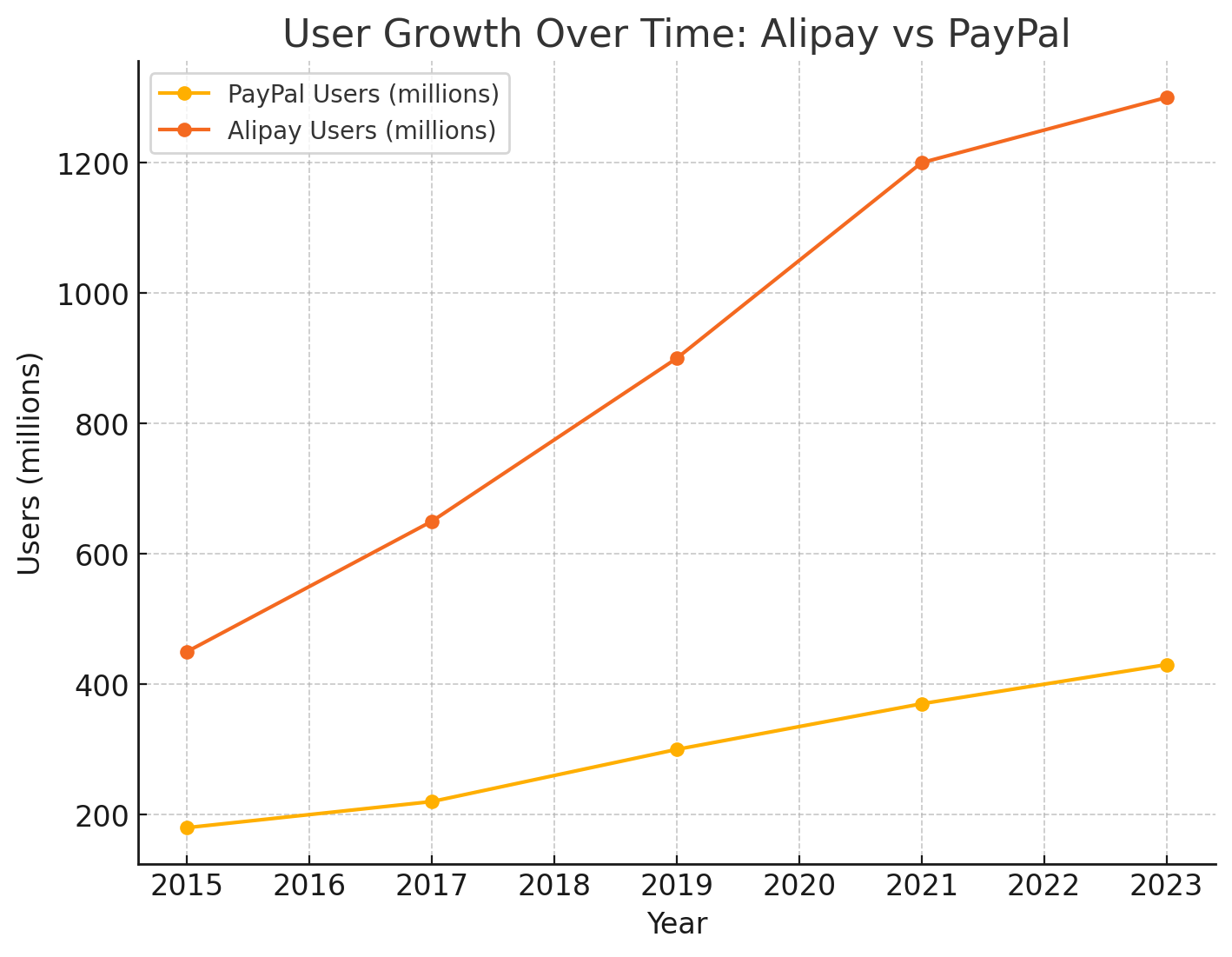

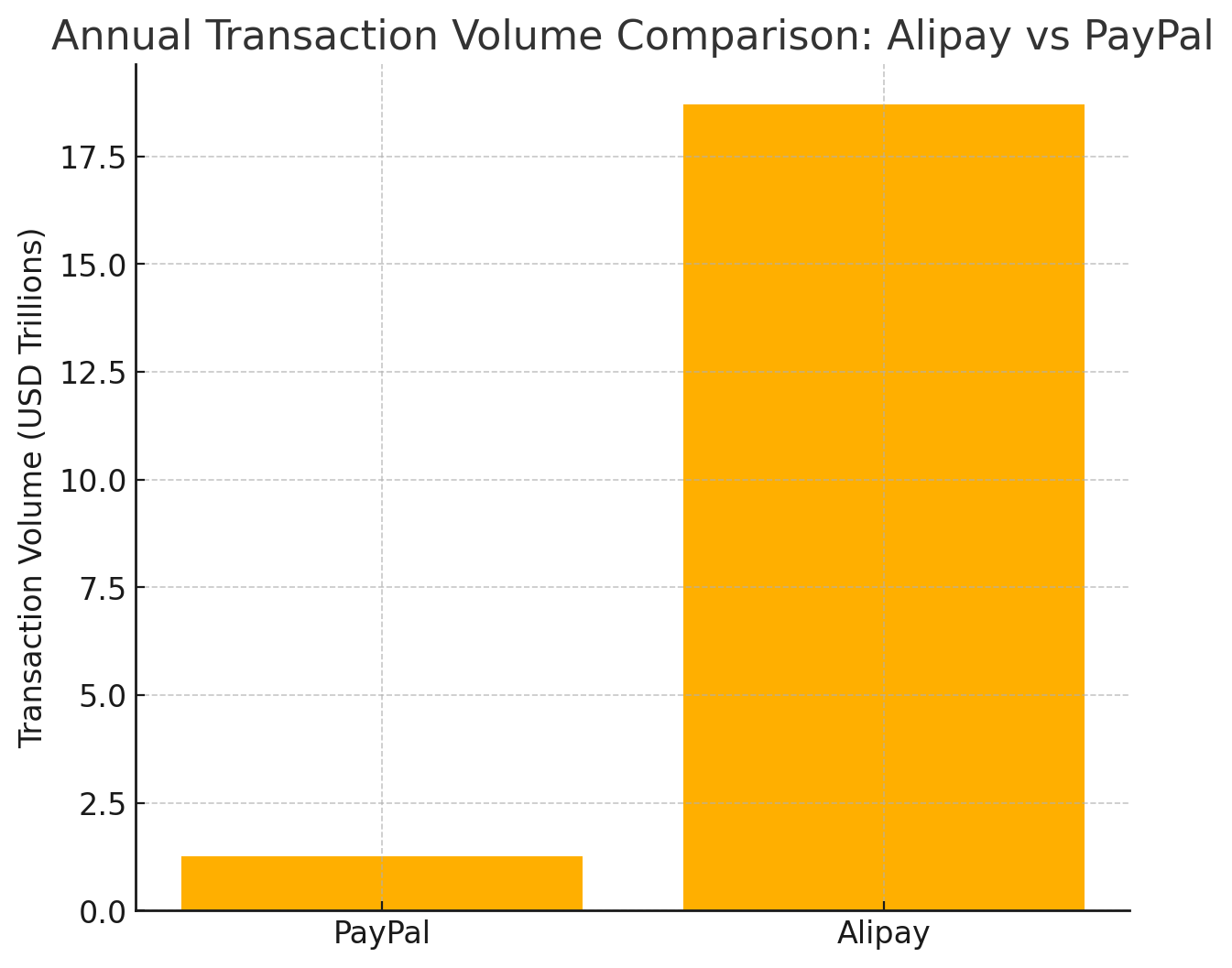

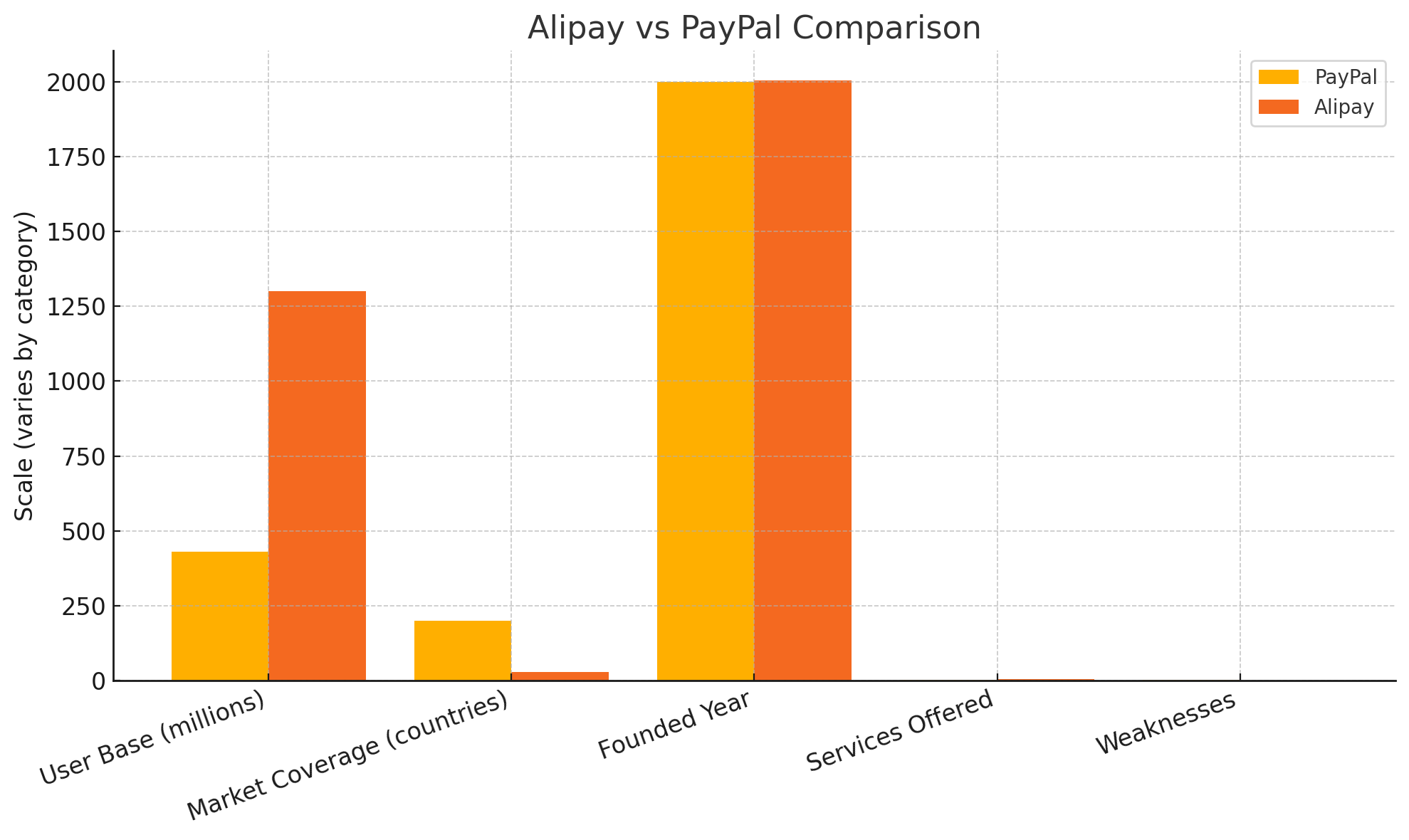

PayPal was founded in December 1998 as Confinity, a software company focused on security for handheld devices. Later, in 2000, it merged with X.com, an online banking company founded by Elon Musk. Rebranded as PayPal, the company shifted its focus to digital payments, becoming one of the first widely accepted online transaction platforms. By 2002, PayPal went public and was quickly acquired by eBay, becoming the default payment solution for millions of online sellers and buyers. Today, PayPal operates in over 200 markets, with more than 430 million active users worldwide.

Birth and Expansion of Alipay

In contrast, Alipay was founded in 2004 by Alibaba Group as an escrow-based payment platform designed to build trust between buyers and sellers on Alibaba’s e-commerce platforms. Over time, Alipay transformed into a super-app, integrating not only payments but also wealth management, credit scoring, loans, insurance, and even social services. Today, Alipay serves over 1.3 billion users, primarily in China and Southeast Asia, making it the world’s largest mobile payment platform.

Market Reach and User Base

PayPal’s Global Dominance

PayPal has established itself as a truly global payment provider. With support for 100+ currencies, PayPal caters to freelancers, small businesses, and international consumers. Its stronghold lies in the U.S., Europe, and parts of Latin America, where it is considered a reliable and secure online payment method.

Alipay’s Command in Asia

Alipay, on the other hand, commands the Asian market with unmatched dominance. Its ecosystem is deeply integrated into everyday life in China, from street food vendors to luxury malls. While Alipay is expanding abroad, particularly in Southeast Asia, its international footprint is still limited compared to PayPal due to regulatory barriers.

Technology and Innovation

PayPal’s Security and Innovation Track

PayPal’s strength lies in its security-first approach and its ability to adapt to global fintech trends. The company has invested heavily in fraud detection, encryption technology, and two-factor authentication. PayPal’s Buyer Protection and Seller Protection programs are unique selling points, reassuring both consumers and businesses that disputes will be fairly resolved.

In recent years, PayPal has expanded into cryptocurrency transactions, allowing users to buy, sell, and hold Bitcoin, Ethereum, and other digital currencies directly on its platform. This move positions PayPal as a forward-thinking player ready to embrace the decentralized future of finance.

Alipay’s Super-App Ecosystem

Alipay is not just a payment solution — it is an entire digital lifestyle ecosystem. The app integrates QR code payments, utility bill payments, ride-hailing, food delivery, ticket booking, healthcare access, and even government services. With the inclusion of Ant Financial’s services, Alipay has also become a key platform for microloans, savings, and insurance.

One of Alipay’s biggest innovations is the social credit scoring system, which evaluates a user’s financial behavior and grants access to services accordingly. Unlike PayPal, Alipay has succeeded in embedding itself into the daily routine of billions, making it more than just a wallet.

Business Models Compared

PayPal’s Transaction-Oriented Model

PayPal primarily earns revenue through transaction fees on online purchases, money transfers, and currency conversions. Merchants pay PayPal a small percentage of each transaction, which has been a sustainable model since e-commerce took off globally. Additionally, PayPal earns from services such as PayPal Credit and partnerships with financial institutions.

However, critics argue that PayPal’s fees are relatively high for small businesses and freelancers, sometimes making it less attractive compared to other local alternatives.

Alipay’s Ecosystem-Driven Model

Alipay’s business model is significantly more diverse. While it earns from payment processing, its true strength lies in the integration of financial services. Ant Group, Alipay’s parent company, generates revenue through wealth management products, lending, and insurance. This ecosystem approach allows Alipay to thrive even if transaction fees are minimal.

Unlike PayPal, Alipay is less dependent on e-commerce alone, positioning it as a financial superpower in China.

Services and Features

PayPal’s Payment, Transfer, and Credit Services

PayPal offers a range of services:

-

Peer-to-Peer Transfers → Quick and easy global transfers.

-

Merchant Solutions → Payment gateways for e-commerce websites.

-

PayPal Credit → Digital credit line for consumers.

-

Cryptocurrency Integration → Buy, hold, and sell digital currencies.

These services have made PayPal a trusted global brand, particularly for freelancers and international businesses.

Alipay’s Super-App Integration with E-Commerce

Alipay’s features go far beyond payments. Some of its key offerings include:

-

QR Code Payments → Used universally in China.

-

Integration with Taobao & Tmall → Alibaba’s marketplaces.

-

Yu’e Bao → The world’s largest money market fund, allowing users to earn interest.

-

Sesame Credit → A credit scoring system integrated into lifestyle activities.

-

Microloans and Insurance → Accessible to individuals and small businesses.

In short, Alipay operates as a one-stop shop for financial and lifestyle needs, making it far more comprehensive than PayPal.

Security and Trust

How PayPal Ensures Global Trust

PayPal has positioned itself as a global benchmark for online trust. With strong encryption, dispute resolution, and fraud detection systems, PayPal is the default payment choice for millions of online buyers. Its Buyer Protection Policy ensures refunds in cases of fraud or non-delivery.

For merchants, PayPal offers Seller Protection, which covers unauthorized payments and chargebacks. This dual-protection system has been crucial in building PayPal’s reputation worldwide.

Alipay’s Risk Management in China and Beyond

Alipay uses big data analytics and artificial intelligence to monitor transactions and prevent fraud. Since it operates primarily in China, where digital payments dominate daily life, Alipay has built advanced real-time risk management tools.

However, concerns exist regarding privacy and government surveillance, as Alipay shares some data with Chinese authorities. This creates hesitation among international users who prioritize data protection.

Regulatory Challenges

PayPal’s Compliance in International Markets

Operating in over 200 markets, PayPal faces complex regulatory requirements. It must comply with anti-money laundering (AML) laws, Know Your Customer (KYC) policies, and financial conduct regulations. While this compliance ensures credibility, it also slows down expansion into certain regions.

Alipay’s Struggles with Global Expansion

Alipay has found it difficult to expand outside Asia due to regulatory hurdles and trust issues. In the U.S. and Europe, Alipay is not as widely accepted due to concerns over Chinese tech dominance and data privacy. Moreover, the halted Ant Group IPO in 2020 highlighted regulatory pressure from the Chinese government itself.

Customer Experience

PayPal’s Simplicity and Universal Reach

One of PayPal’s strongest assets is its simplicity. For most users, PayPal requires only an email address and a linked bank account or card. Transactions are straightforward and internationally recognized, making it a go-to platform for freelancers, online shoppers, and global businesses.

The universality of PayPal cannot be overstated. From e-commerce giants like eBay and Shopify to small independent stores, PayPal is widely supported. Its global reach ensures that users can transact almost anywhere in the world without worrying about compatibility.

However, user complaints often revolve around:

-

High transaction fees

-

Frozen accounts without clear explanations

-

Delays in fund withdrawals

These issues create friction in what is otherwise a smooth customer journey.

Alipay’s Immersive Super-App Experience

In contrast, Alipay provides a deeply immersive customer experience. Its integration into everyday activities means that for many Chinese users, life without Alipay is unimaginable. From ordering food to paying utility bills, everything happens within one app.

The user interface is intuitive and designed to keep people engaged. Unlike PayPal, which is primarily transactional, Alipay offers a lifestyle experience, seamlessly connecting finance with social and personal needs.

However, for international users, Alipay can feel overwhelming and restrictive, especially since many of its features are locked behind Chinese residency or a Chinese bank account.

Financial Inclusion

PayPal’s Role in Freelancers and SMEs

PayPal has played a vital role in financial inclusion globally. For freelancers, especially in developing countries, PayPal provides access to international markets that would otherwise be closed. Platforms like Upwork, Fiverr, and Etsy heavily rely on PayPal for payments, enabling millions to earn across borders.

For small and medium-sized enterprises (SMEs), PayPal’s merchant services make cross-border trade more accessible. By lowering barriers, PayPal has empowered entrepreneurs in Africa, South Asia, and Latin America.

Still, limited coverage in countries like Pakistan, Bangladesh, and some African nations restricts PayPal’s full potential for global financial inclusion.

Alipay’s Role in Rural China and Developing Asia

Alipay has been revolutionary in China’s rural areas, where traditional banking infrastructure is limited. By enabling mobile-based microtransactions, Alipay has provided access to credit, insurance, and savings for millions who were previously excluded from formal banking.

The Yu’e Bao program, which allows users to invest spare change into money market funds, has been a game-changer for grassroots savings. Additionally, Alipay’s partnerships in Southeast Asia (with companies like GCash in the Philippines) extend financial inclusion beyond China.

Counter-Arguments: Weaknesses of Each System

PayPal’s High Fees and Limited Features

Despite its global dominance, PayPal faces criticism for:

-

High fees for international transactions (often 3–5% plus conversion costs).

-

Account freezing policies, which frustrate small businesses.

-

Limited features compared to super-apps like Alipay.

Thus, while PayPal is reliable, it can be expensive and inflexible.

Alipay’s Dependence on Chinese Market

Alipay’s biggest weakness is its over-reliance on China. Outside Asia, adoption is limited due to:

-

Regulatory restrictions in the West.

-

Concerns over data security and Chinese government surveillance.

-

Complex onboarding for foreigners.

This makes Alipay appear regionally dominant but globally restrained, unlike PayPal’s worldwide presence.

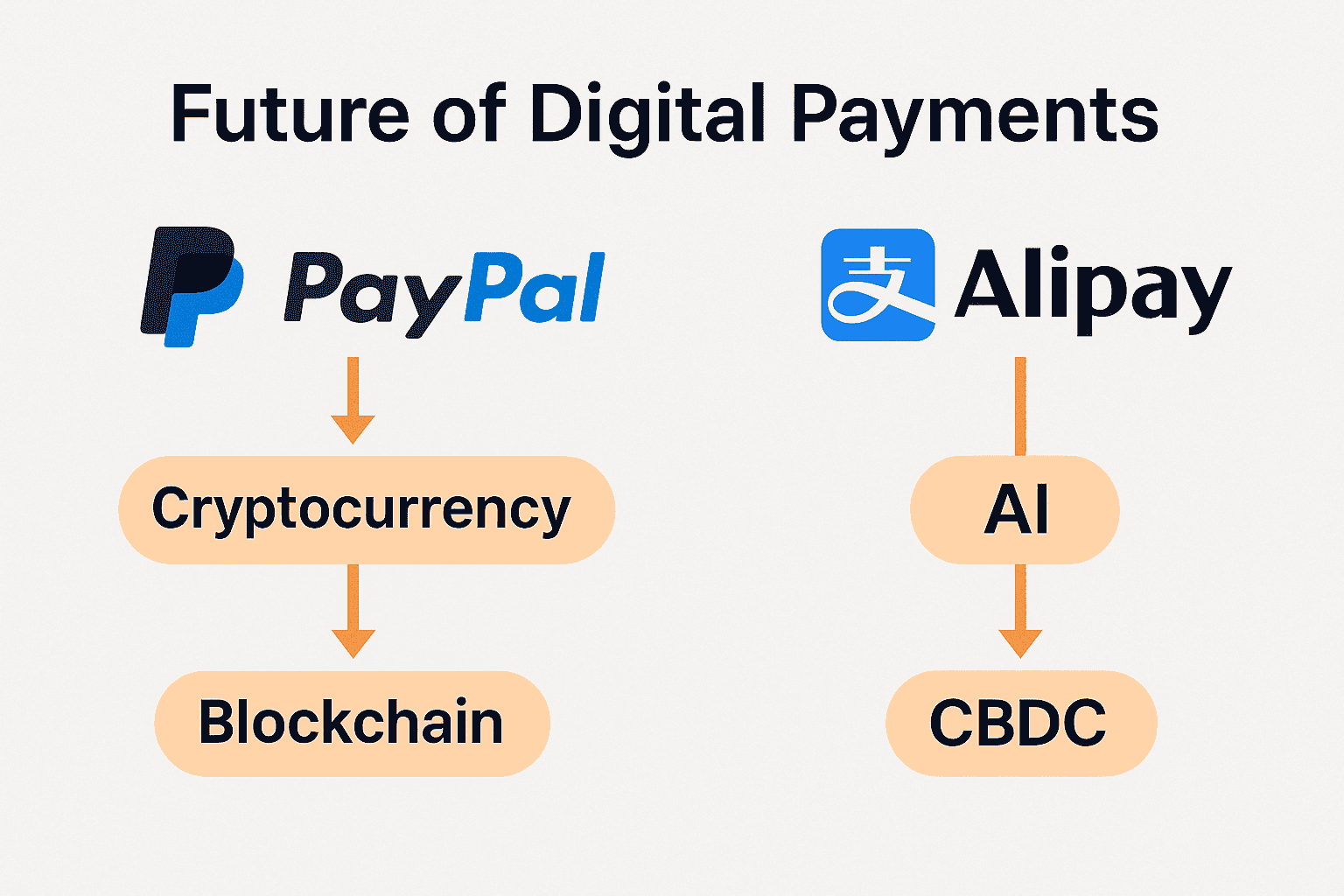

Future of Digital Payments

Global Trends in Cashless Societies

The world is rapidly moving towards cashless economies. By 2030, digital payments are expected to surpass cash transactions globally. Both PayPal and Alipay are positioning themselves as leaders in this transformation.

-

PayPal → Focused on expanding cryptocurrency adoption, global merchant solutions, and cross-border payments.

-

Alipay → Expanding financial ecosystems into health, education, and AI-driven credit scoring.

Blockchain, AI, and Fintech Integration

Emerging technologies will redefine digital payments:

-

Blockchain → Decentralized payments challenge both PayPal and Alipay.

-

AI → Advanced fraud detection and personalized financial services.

-

Central Bank Digital Currencies (CBDCs) → Countries like China are already testing the Digital Yuan, which could integrate with Alipay.

The future will likely see hybrid systems, where PayPal and Alipay must adapt to coexist with decentralized fintech innovations.

Case Studies

PayPal in the U.S. and Europe

In the U.S., PayPal is a dominant force in e-commerce, powering platforms like eBay, Etsy, and Shopify. Its partnerships with Venmo (peer-to-peer transfers) and its entry into cryptocurrency trading solidify its stronghold.

In Europe, PayPal benefits from regulatory frameworks that encourage digital payments, but faces competition from local players like Klarna and Revolut.

Alipay in China and Southeast Asia

Alipay’s success story is most evident in China, where cash transactions are nearly obsolete. From luxury malls in Beijing to food stalls in rural villages, QR-based Alipay payments dominate.

In Southeast Asia, Alipay’s strategy is partnerships. Collaborations with wallets like GCash (Philippines), Dana (Indonesia), and Touch ’n Go (Malaysia) expand its reach. However, outside Asia, Alipay still struggles to penetrate mainstream markets.

Comparative Table: Alipay vs PayPal

| Feature | PayPal | Alipay |

|---|---|---|

| Founded | 1998 (U.S.) | 2004 (China) |

| Users | ~430 million | ~1.3 billion |

| Primary Market | Global (200+ countries) | China & Southeast Asia |

| Business Model | Transaction-based | Ecosystem-driven |

| Key Services | Online payments, credit, crypto | Super-app: payments, loans, savings |

| Security | Buyer & Seller Protection | AI-based fraud detection |

| Weakness | High fees, account freezes | Over-reliance on China |

| Innovation | Crypto integration | Super-app + Credit Scoring |

| Future Focus | Cross-border + blockchain | AI + CBDC integration |

FAQs

Is Alipay safer than PayPal?

Both platforms are secure, but PayPal has stronger global consumer protection policies, while Alipay excels in AI-driven fraud detection within China.

Can foreigners use Alipay?

Yes, but with restrictions. Foreigners in China can link international cards to Alipay, but outside China, access is limited.

Which is better for businesses, Alipay or PayPal?

For global businesses, PayPal is better due to worldwide coverage. For businesses targeting Chinese consumers, Alipay is the clear winner.

Does PayPal work in China?

PayPal has limited operations in China and is overshadowed by Alipay and WeChat Pay.

What are the main disadvantages of PayPal?

High fees, account freezing, and slower withdrawal processes compared to competitors.

What makes Alipay unique compared to PayPal?

Alipay’s super-app ecosystem integrates lifestyle, finance, and social services — something PayPal doesn’t offer.

Conclusion and Recommendations

Summarizing the Clash

The comparison of Alipay vs PayPal reveals two very different fintech philosophies:

-

PayPal is a global pioneer in online payments, thriving on simplicity and universal reach.

-

Alipay is a regional powerhouse, redefining what a financial app can do through its ecosystem model.

Final Recommendations for Users and Businesses

-

Global Freelancers & SMEs → PayPal is the better option due to international acceptance.

-

Chinese and Asian Market Businesses → Alipay is essential for reaching billions of users.

-

Future Outlook → Both must adapt to blockchain, AI, and digital currencies or risk being disrupted by decentralized alternatives.

difficult to expand outside Asia due to regulatory hurdles and trust issues. In the U.S. and Europe, Alipay is not as widely accepted due to concerns over Chinese tech dominance and data privacy. Moreover, the halted Ant Group IPO in 2020 highlighted regulatory pressure from the Chinese government itself.