Introduction

In today’s fast-moving digital trade era, global buyers frequently face a common dilemma: Should I pay my Chinese suppliers through a credit card or use Alipay instead?

When importing products from platforms like Alibaba, AliExpress, or 1688, payment reliability and trust are paramount. While international cards appear convenient, they often come with hidden costs, delayed settlements, and bank restrictions. On the other hand, Alipay — China’s leading fintech platform under the Alibaba Group — offers an ecosystem built precisely for cross-border trade security, low fees, and direct supplier connections.

This article examines why it’s often smarter and safer to use Alipay instead of credit card when sending payments to Chinese suppliers, highlighting the system’s pros, cons, and global efficiency for importers and small traders.

The Problem with Paying Suppliers via Credit or Debit Cards

Credit and debit cards were built for consumer purchases — not for international B2B trade. When foreign buyers use them on platforms like Alibaba, several issues emerge:

-

High International Fees: Banks charge 2–5% in conversion and processing fees. Some even add cross-border surcharges that make small orders expensive.

-

Currency Conversion Delays: Converting USD or PKR into RMB involves multiple banks and intermediary channels, often delaying supplier receipts by 3–5 days.

-

Rejection or Fraud Alerts: Because many Chinese suppliers don’t have direct card terminals, transactions may fail due to “unrecognized merchant” alerts.

-

Lack of Escrow Protection: Unlike Alipay’s trade assurance, card payments rely on bank chargebacks — which are slow, uncertain, and usually favor the seller’s country.

-

Limited Acceptance in China: Most Chinese wholesalers or manufacturers do not use Visa or MasterCard; they rely on Alipay or WeChat Pay for 95% of domestic transactions.

Thus, what looks like a modern global payment tool often becomes a barrier in real Chinese commerce.

Why You Should Use Alipay Instead of Credit Card

The key advantage lies in the ecosystem alignment. Alipay isn’t just a wallet — it’s the default payment layer across Alibaba’s marketplace, Taobao, 1688, and even factory-level transactions.

a. Instant Settlement and Lower Fees

When you use Alipay instead of credit card, your payment goes directly to the supplier’s Alipay wallet in RMB.

There’s no foreign exchange chain, no intermediary banks, and settlement occurs within seconds or minutes, not days.

Transaction fees are minimal compared to 2–5% card charges, making Alipay especially beneficial for bulk or repeat orders.

b. Better Exchange Rate

Alipay applies real-time mid-market exchange rates, much fairer than bank card conversion rates. For every $1,000 payment, buyers can save $20–$50 just through exchange optimization.

c. Built-In Escrow Protection

When you send funds through Alipay’s Trade Assurance, the payment is held in escrow until the supplier ships and you confirm receipt.

This mechanism is far safer than relying on credit card disputes, which can take weeks.

d. Seamless Integration with Alibaba Ecosystem

Alipay is deeply tied to Alibaba, AliExpress, and 1688. That means every step — from invoicing to shipment confirmation — updates automatically within the same system.

Buyers enjoy automated receipts, refund tracking, and dispute resolution, something cards cannot provide.

e. Enhanced Trust Among Suppliers

Chinese vendors prefer clients who use Alipay. It signals serious intent and familiarity with local business culture.

Suppliers often offer discounts or faster delivery to Alipay users because the system ensures funds security and transparency.

Pros of Using Alipay for International Buyers

| Advantages | Explanation |

|---|---|

| Low Fees | Usually 0–1.5% compared to 3–5% for cards. |

| Real-Time Exchange | RMB conversion happens instantly with transparent rates. |

| Escrow Security | Alipay holds funds until goods are shipped. |

| Speed | Payment confirmation within seconds. |

| Trust Factor | Highly respected by Chinese suppliers. |

| Refund Flexibility | Refunds go straight to your balance without bank disputes. |

| Mobile & Global | Works via app or web, globally available. |

When you use Alipay instead of credit card, you’re essentially participating in China’s native financial system, where 1 billion+ users transact daily.

Limitations or Cons of Using Alipay

While Alipay offers many advantages, international traders should also understand its limitations:

a. Account Verification Outside China

Foreign users must verify their Alipay account using passport, phone number, and sometimes proof of business. The process can take a few days but is essential for higher transfer limits.

b. Currency Restrictions

Some foreign accounts may not directly hold RMB. They might need to top up using third-party exchangers or linked accounts (e.g., Wise, Payoneer, or local partners).

c. Documentation for Large Transfers

For high-value transfers, Alipay may request invoice proof or business purpose to comply with China’s foreign exchange laws.

d. Ecosystem Limitation

Outside Alibaba or Chinese supplier circles, Alipay isn’t as widely accepted as Visa or Mastercard for retail payments. Hence, it’s best suited for business-to-business trade.

Despite these, for importers dealing with suppliers in China, the pros far outweigh the cons.

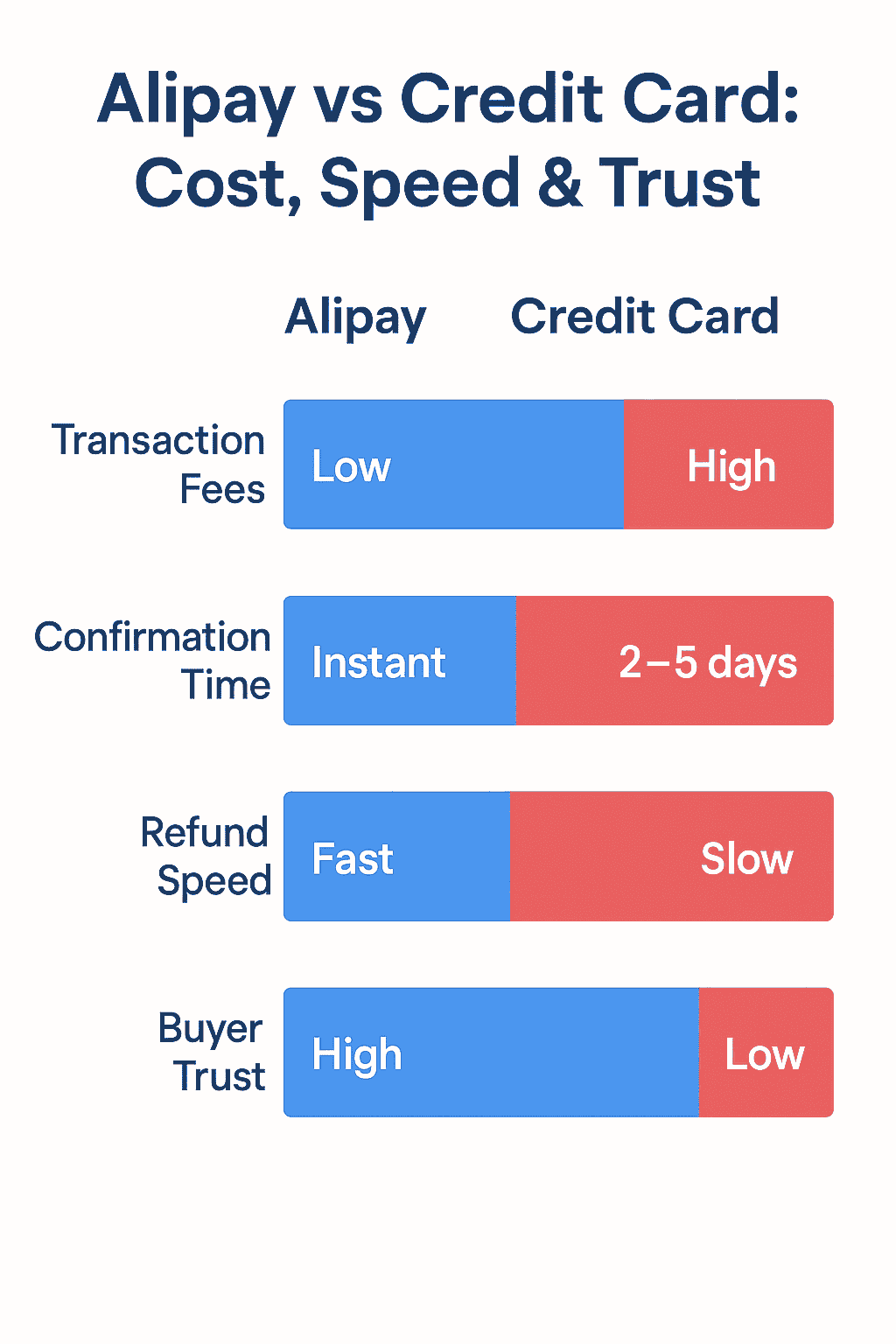

Cost & Security Comparison: Alipay vs Credit Card

| Feature | Alipay | Credit/Debit Card |

|---|---|---|

| Transaction Fee | 0–1.5% | 3–5% |

| Exchange Rate | Real-time mid-market | Bank conversion |

| Speed | Instant (seconds) | 2–5 days |

| Buyer Protection | Escrow (Trade Assurance) | Chargeback (weeks) |

| Supplier Acceptance | Very high | Limited |

| Refund Handling | Direct & digital | Bank-dependent |

| Risk of Decline | Low | High (cross-border blocks) |

Example Scenario: Paying a Supplier on Alibaba

Let’s imagine you’re importing 50 smartphone accessories worth $800 from Shenzhen.

-

Using Credit Card:

Your bank adds 3.5% foreign transaction + poor exchange rate. The supplier receives only ~$760 after deductions. Payment may take 2–3 working days, and the vendor might delay shipment until the funds clear. -

Using Alipay:

You top up or link your balance, pay instantly through Alipay escrow. Supplier receives confirmation within seconds and ships next day. If any issue arises, funds remain protected until resolution.

The difference is not only in cost but in trust and transaction flow — the two factors that define smooth cross-border trade.

Why Chinese Suppliers Prefer Alipay

For Chinese merchants, Alipay is not just a wallet; it’s a business identity tool that validates payments, ensures tax compliance, and automates accounting.

This is why when you use Alipay instead of credit card, suppliers:

-

Ship faster, knowing the money is securely held.

-

Trust you more, as you use their native payment culture.

-

Avoid foreign bank friction, helping them focus on your order.

Hence, Alipay isn’t only a payment tool — it’s a relationship builder between foreign buyers and Chinese manufacturers.

Conclusion

In global trade, payment confidence defines partnership success. When you pay a Chinese supplier through Alipay instead of credit card, you remove unnecessary intermediaries, delays, and currency losses. You also enter a fintech ecosystem designed for trust, transparency, and real-time efficiency.

For any importer or small trader dealing with Alibaba or AliExpress, Alipay stands out as the smarter, safer, and more economical choice.

As China leads the world toward digital trade integration, aligning your payment habits with its ecosystem gives you not only better rates — but a competitive edge in speed and reliability.