Introduction

“Scan and pay” is the most ordinary gesture in modern China: a phone camera glances at a black-and-white square, a soft chime rings, and value moves. Beneath that simple ritual sits a dense stack of standards, encryption, tokenization, merchant onboarding flows, risk engines, and settlement ledgers. In this blog, we analyze the QR code—its definition and anatomy, how Alipay QR Codes payments actually work end-to-end, why QR triumphed over cards in China, what the merchant-presented (MPQR) and customer-presented (CPQR) models really do, and how Alipay embeds trust, speed, and scale into those tiny squares.

QR codes won because they reduce friction for every stakeholder—consumers, street vendors, and platforms. Alipay industrialized QR by combining four pillars: standardized data payloads, instant authentication, dynamic risk control, and predictable settlement. The result is a low-cost, high-reach payment fabric.

Part I — QR Codes 101: The Building Blocks

What is a QR Code?

A QR (Quick Response) code is a two-dimensional barcode with modules (black/white squares) encoding data—usually a URL or structured text. It supports error correction (L/M/Q/H), meaning it still scans if partially damaged.

Anatomy of a typical QR:

-

Finder patterns (three big squares) for fast alignment.

-

Timing patterns to keep rows/columns in sync.

-

Format/version info (error correction level, mask).

-

Data + error-correction codewords.

Why QR for payments?

-

Ubiquity: Any camera can scan.

-

Cost: No special hardware for the buyer; for the seller, a printed poster or a tiny speaker device (Alipay Soundbox) can suffice.

-

Speed + Offline Resilience: Works with intermittent connectivity (static merchant QR still displays even if the phone is briefly offline; token validation completes when the network returns).

Part II — Two Payment Models: MPQR vs CPQR

When people say “scan the Alipay,” they usually mean one of two flows:

-

Merchant-Presented QR (MPQR)

The merchant shows a QR. The customer scans it with Alipay, enters/confirm the amount (if not encoded), authorizes, and the payment posts. -

Customer-Presented QR (CPQR)

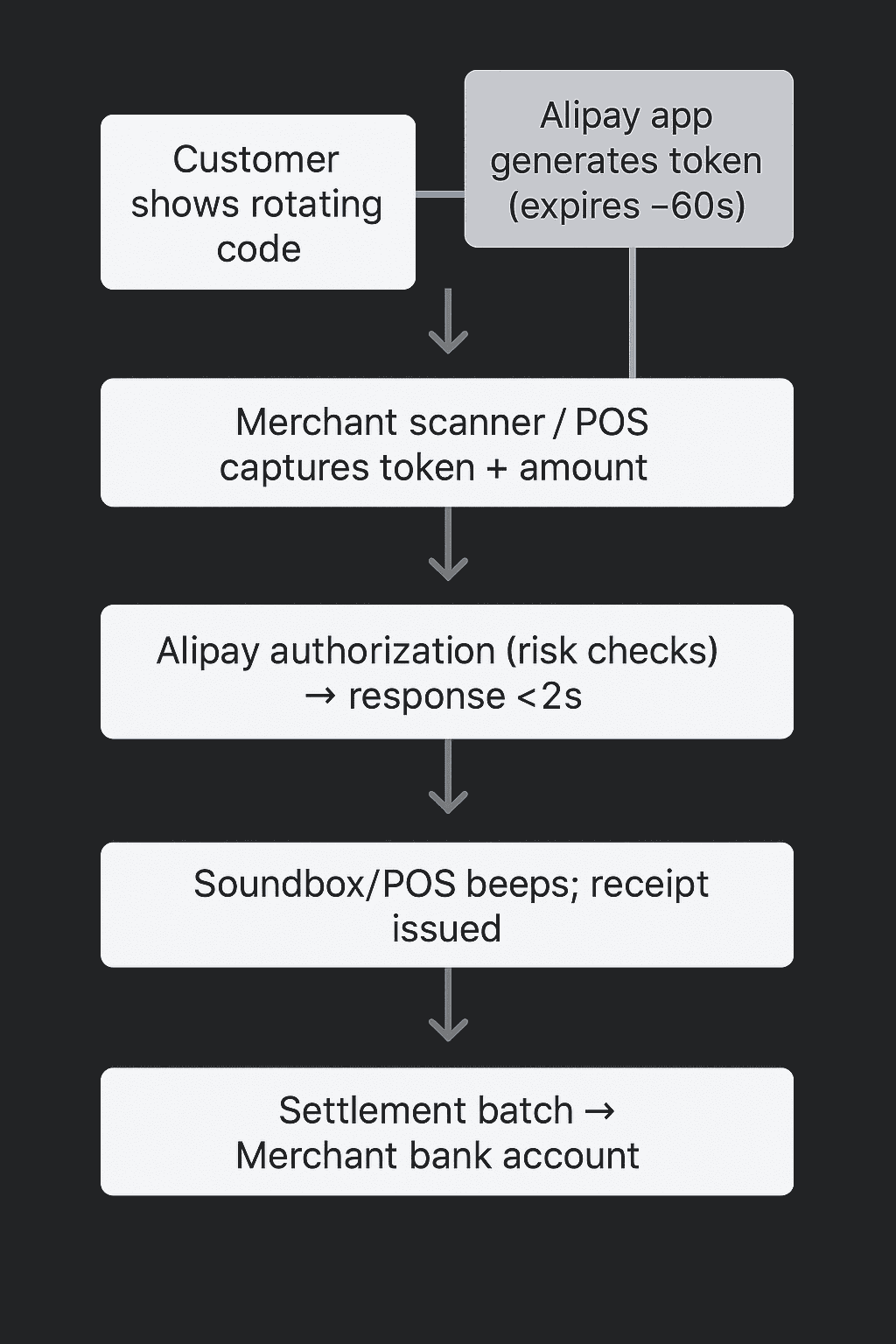

The customer shows their personal Alipay payment code (a rotating token). The merchant scans it with a scanner/POS/Soundbox, requests funds, and gets an approval beep.

Quick compare:

| Aspect | MPQR (Merchant shows QR) | CPQR (Customer shows code) |

|---|---|---|

| Who scans? | Customer | Merchant |

| Code type | Static or dynamic merchant QR | Dynamic customer token (rotates every ~60s) |

| Typical use | Street stalls, tip jars, posters | Supermarkets, pharmacies, transit |

| Amount entry | Customer enters if not pre-filled | Merchant/POS sends amount in request |

| Speed | Fast | Often fastest (one tap + scan + beep) |

| Hardware | Poster or Soundbox | Scanner/POS or Soundbox |

Part III — Static vs Dynamic (and Why It Matters)

Static Merchant QR:

-

Printed once; encodes merchant ID / payment link.

-

Amount may be entered manually by the payer.

-

Cheapest to deploy; perfect for micro-merchants and pop-ups.

Dynamic Merchant QR:

-

Generated fresh per transaction; encodes merchant ID + exact amount + transaction nonce.

-

Reduces miscoding and fraud; great for checkout kiosks or order-ahead.

Customer Dynamic Code (for CPQR):

-

Rotates frequently (time-based token).

-

Minimizes replay risk—if someone screenshots it, it will expire.

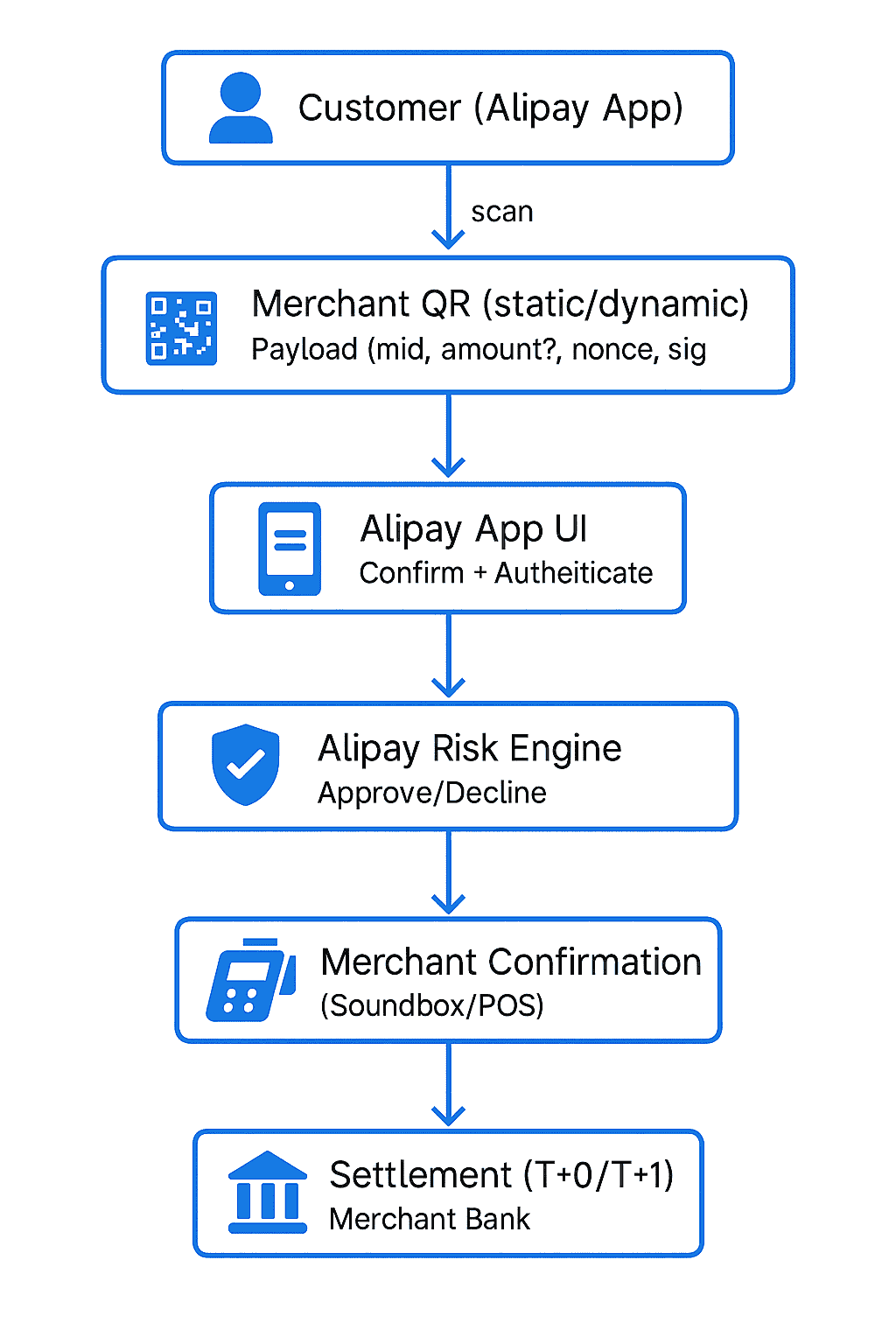

Part IV — The Alipay QR Payload: What’s Inside the Square?

While exact field names vary by environment and partner, a typical Alipay MPQR payload encodes:

-

Merchant identity (mid + optional store/terminal IDs) links to onboarding KYC in Alipay’s acquiring system.

-

Amount may be absent in static codes; present in dynamic codes.

-

Nonce + timestamp defeat replay.

-

Signature authenticates origin.

For CPQR, the code represents a short-lived token tied to the user’s wallet; the merchant device sends an online authorization to Alipay including amount + merchant details + token.

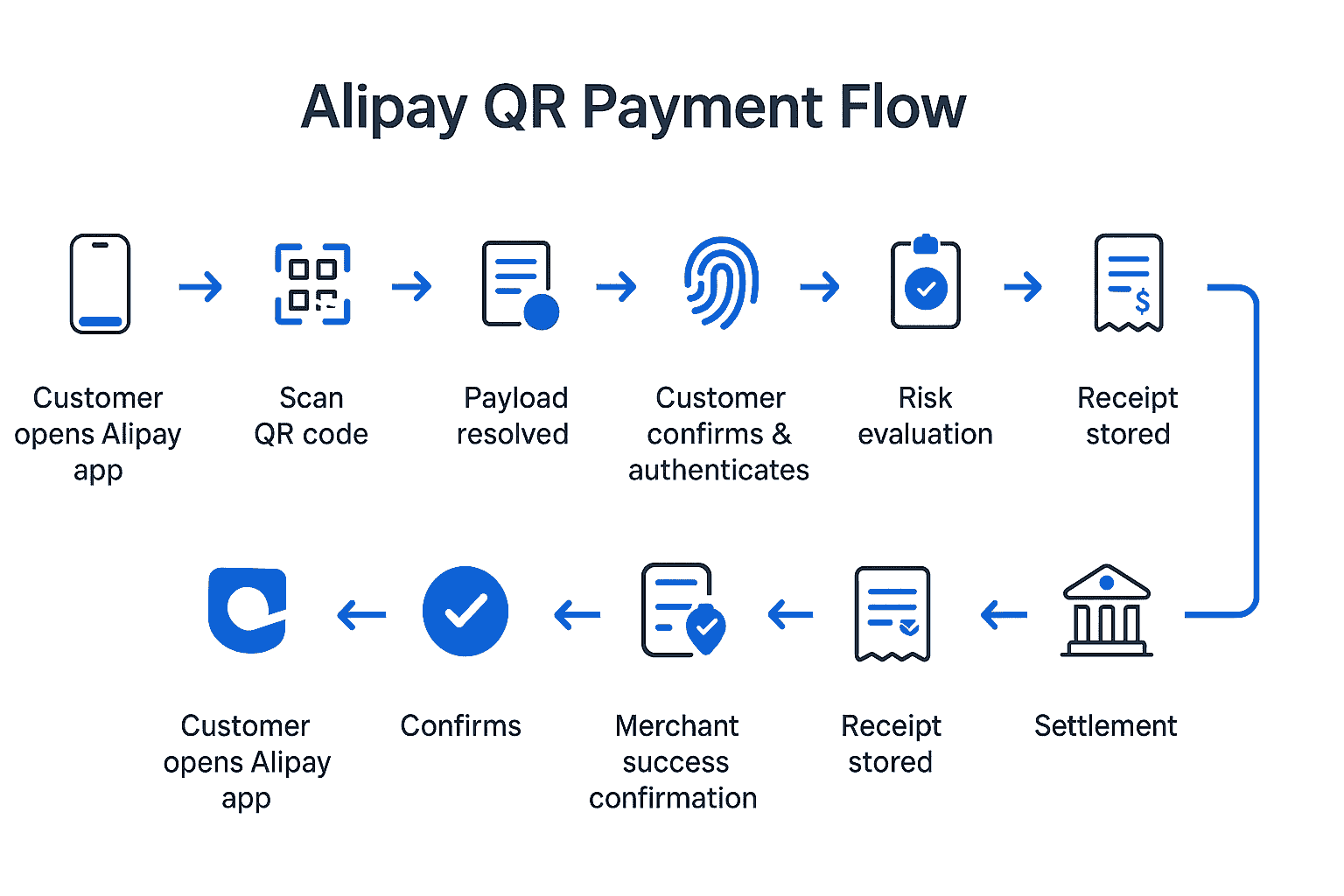

Part V — The End-to-End Payment Flow (Alipay)

A) Merchant-Presented QR (Customer Scans)

Security + UX:

-

If a static QR lacks amount, the customer enters the amount. Alipay displays merchant legal name to prevent misdirection.

-

Biometric/PIN protects the wallet.

-

Risk engine considers device fingerprint, location, historical pattern, and merchant profile.

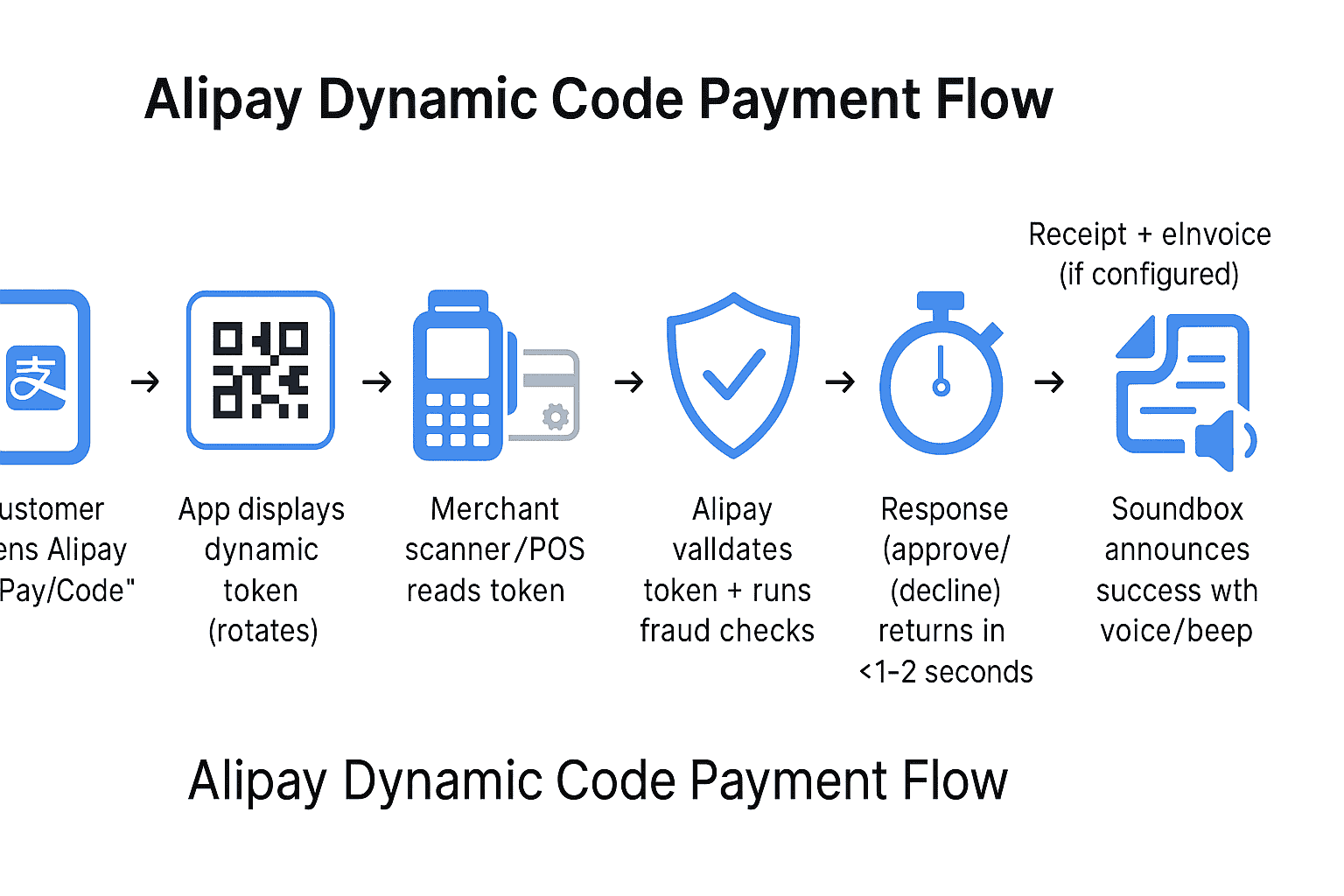

B) Customer-Presented QR (Merchant Scans)

Why CPQR is popular at grocers: cashier controls the amount; the buyer simply shows code. It’s as fast as swiping a card—but cheaper infrastructure.

Part VI — The Risk & Trust Stack (Why People Are Comfortable Paying a QR)

-

Strong Customer Authentication (SCA).

PIN, fingerprint, face ID in the Alipay app. -

Tokenization and Expiry.

CPQR uses rotating tokens; MPQR dynamic codes use nonces. -

Merchant KYC & Onboarding.

Alipay/its acquirers verify business licenses, bank accounts, responsible officers, and MCC (merchant category code). High-risk categories have stricter controls. -

Behavioral Risk Engine.

Rules + machine learning: sudden large first-time payments, mismatched geolocation, device anomalies → challenge or decline. -

Liveness & Tamper Signals.

The app monitors OS integrity, rooted devices, emulator patterns. -

Clear Receipts + Dispute Workflows.

In-app receipts, merchant statements, and refund / after-sale channels build confidence.

Part VII — The Money Rails: Authorization, Clearing, Settlement

Authorization:

-

Real-time decision (approve/decline) at Alipay.

Clearing:

-

Alipay aggregates a merchant’s day’s transactions into a batch.

Settlement:

-

Funds move per contract, often T+1 (next business day) to merchant’s linked bank account. Some categories/partners can be T+0 (same day) with fees.

Fees:

-

Merchant Discount Rate (MDR) is typically far lower than card rails due to simpler infrastructure and domestic scale.

-

Micro-merchants get preferential rates to promote inclusion.

Part VIII — Hardware in the Wild: From Paper to Soundbox

-

Paper Tent/Poster: cheapest MPQR.

-

LCD QR Stands: generate dynamic QR and show “Paid ¥X.”

-

Alipay Soundbox: tiny speaker connected to merchant app/cloud; speaks “Payment received ¥X” in real time, even if the cashier isn’t watching a screen.

-

Barcode Scanners/POS: for CPQR at larger retailers.

Why Soundbox matters: It closes the loop audibly—no disputes about whether payment arrived. Great for busy wet markets or night stalls.

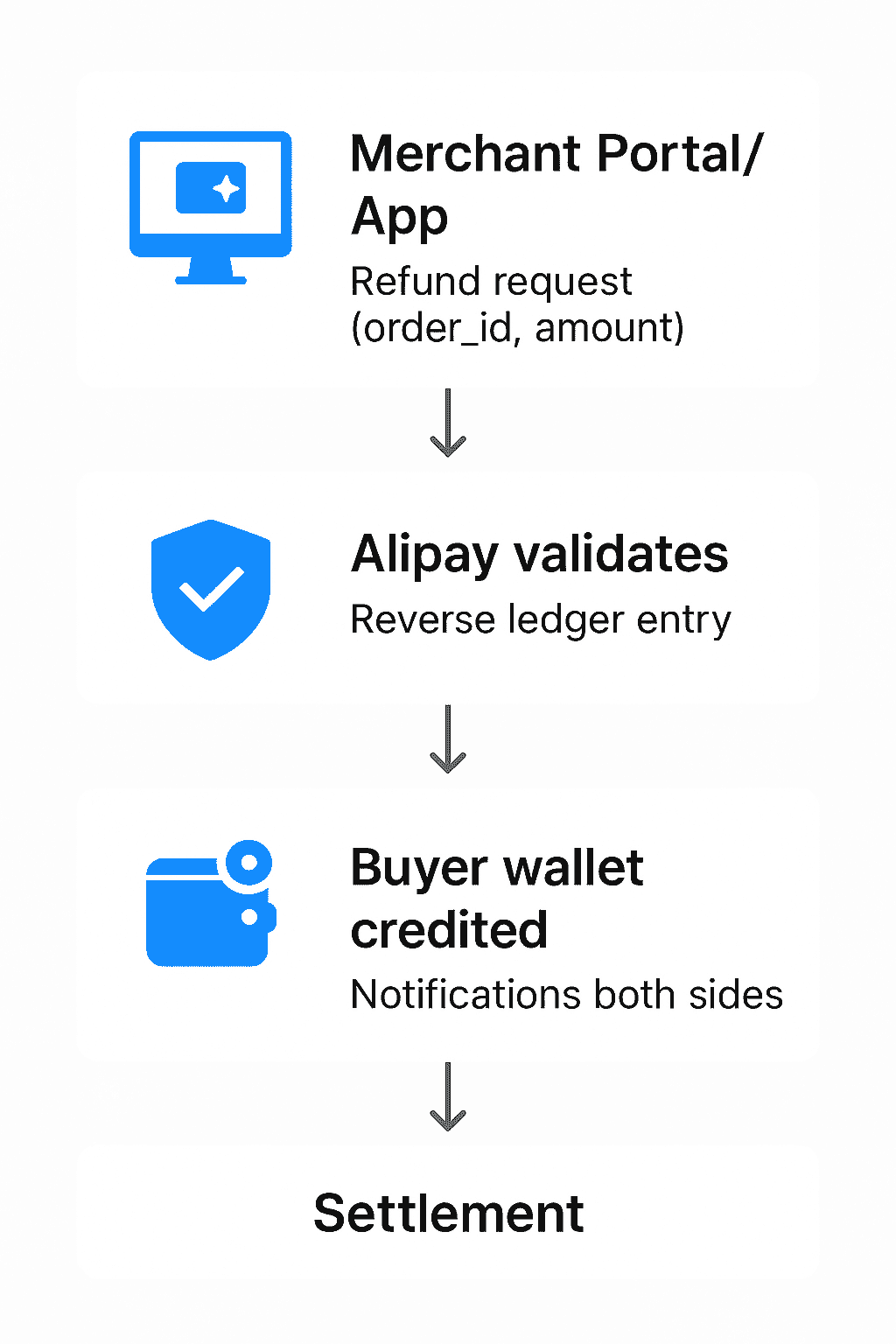

Part IX — Refunds, Reversals, and Disputes

-

Instant Refunds: Merchant can initiate in their merchant app/portal; Alipay credits the buyer’s wallet quickly.

-

Partial Refund: Supported when the buyer returns one item out of several.

-

Dispute Handling: If buyer claims wrong merchant or duplicate charge, Alipay investigates with transaction logs, token traces, device/time stamps.

-

Chargebacks? QR ecosystems don’t mirror card-scheme chargebacks 1:1; but there are structured after-sale mechanisms and compliance-driven reversals.

Part X — Why QR Beat Cards in China (Cause-Effect Analysis)

Cause 1: Low card/POS penetration → Effect: QR lowered hardware costs

Merchants printed a code and were live.

Cause 2: Marketplace growth (Taobao/Tmall) → Effect: escrow & wallet culture

Trust built inside platforms, not at bank counters.

Cause 3: Mobile-first consumers → Effect: wallets as the default

Biometrics + one-tap flows beat typing PINs on dirty POS pads.

Cause 4: Policy support for inclusion → Effect: micro-merchant enablement

Alipay onboarded small vendors with KYC-lite on compliant rails.

Part XI — Standards and Interoperability (Plain-English Guide)

-

EMVCo QR: global spec for CPQR/MPQR fields (widely referenced by wallets).

-

PBOC / Chinese QR Standards: domestic rules for code formats, content, and risk controls; also guidance on Unified QR so one code can accept multiple wallets.

-

UnionPay QR (Cloud QuickPass): operates alongside Alipay/WeChat; many merchant plates accept all.

Alipay in practice: speaks the local dialect of global QR, ensuring that its codes carry the right merchant identity, amount (if needed), and signatures for quick, safe resolution.

Part XII — Developer View: APIs, Webhooks, and Reconciliation (Conceptual)

For integrated merchants:

-

Create Order (optional for dynamic MPQR): send amount, subject, order_id.

-

Generate QR: receive the QR payload/URL and render as image.

-

Payment Callback (Webhook): Alipay notifies on success with transaction_id, order_id, amount, time.

-

Query API: poll payment status if webhook fails.

-

Refund API: send order_id + amount to trigger refund.

-

Reconciliation: download settlement files; match fees and payouts.

Data hygiene: log order_id ↔ transaction_id, timestamps, amounts, and receipt URLs; this is gold during audits.

Part XIII — Offline & Low-Connectivity Scenarios

-

Static MPQR requires only the payer’s phone to be online. If the merchant is offline, the Soundbox or app receives the confirmation later, but the buyer still pays now.

-

CPQR generally needs merchant connectivity to send the amount + token for approval.

-

Risk fallback: if connectivity blips, Alipay may cache pending confirmations and reconcile when the network returns.

Part XIV — Fraud Patterns and Alipay Countermeasures

Common attempts:

-

QR swap: Fraudster slaps their QR sticker over the merchant’s.

-

Countermeasure: branded plates, glue tags, and merchant-visible Soundbox confirmations (if it doesn’t speak, something’s wrong).

-

-

Replay of CPQR: Snapshot of a user’s code.

-

Countermeasure: rotating tokens; code expires in ~60s.

-

-

Fake success screen: Buyer flashes a forged “paid” screen.

-

Countermeasure: merchant must rely on Soundbox/POS confirmation, not the buyer’s screen.

-

-

Account takeovers: Stolen phone/credentials.

-

Countermeasure: biometrics, device binding, risk challenges.

-

Part XV — Pricing, Economics, and Why SMEs Love QR

-

Lower MDR than cards.

-

Faster payouts improve cashflow.

-

Marketing hooks: coupons, mini-program membership, points—inside the same app.

-

Data visibility: simple dashboards for daily totals, peak hours, repeat buyers.

Result: Even a fruit cart has enterprise-grade payments and analytics.

Part XVI — Compliance, KYC, and Merchant Categories

-

KYC tiers: micro-merchant vs general merchant; documents scale with risk.

-

MCCs (merchant category codes) set risk policies and fee classes.

-

Limits: caps on single transactions or daily volume for certain tiers, lifted with stronger verification.

-

Prohibited categories: enforced at onboarding and through monitoring (triggering reviews/suspensions).

Part XVII — UX Details that Make Alipay Feel “Instant”

-

Prefetching merchant info after QR detection; showing name/logo builds trust.

-

Haptic + audio cues on success.

-

Saved amounts for frequent bills (utilities/parking).

-

Auto-apply coupons or Ant Forest green points (behavioral nudge to keep using).

Part XVIII — Beyond Payments: Loyalty, Invoicing, and Accounting

-

Membership mini-programs tie a scan to points, tiers, birthdays.

-

e-Fapiao (e-Invoice) flows: after payment, capture buyer tax ID and issue digital invoice.

-

Export to accounting: reconciliation files map to ledgers (date, order, tax, fee).

Part XIX — International Use: Tourists and Cross-Border

When abroad:

-

Merchant-presented QR at supported stores resolves to an Alipay open-loop partner; foreign acquirer handles the local leg; Alipay debits the user in CNY with FX.

-

Tax refund and duty-free counters in airports often support Alipay CPQR for speedy checkout.

Key point: Same user habit—scan and confirm—works from Beijing to Bangkok to Berlin (where supported).

Part XX — The Future: Digital Yuan, Unified QR, and Trusted Devices

-

Digital Yuan (e-CNY): Alipay integrates as front-end rails; QR flows remain familiar while settlement anchors to the CBDC ledger.

-

Unified QR plates: one code handling Alipay / WeChat / UnionPay improves merchant simplicity.

-

Trusted devices: next-gen Soundboxes with secure chipsets and voice AI (language, amounts, fraud alerts).

Prediction: the QR square persists, but the payload evolves—more tokenization, CBDC hooks, and on-device risk signals.

Diagrams (Text Renderings)

1) MPQR Payment (Customer Scans Merchant Code)

2) CPQR Payment (Merchant Scans Customer Code)

Best Practices for Merchants (Actionable)

-

Use branded QR plates; inspect daily.

-

Never trust the buyer’s success screen—listen for Soundbox or check your merchant app.

-

Separate cashier and owner logins; 2FA on owner account.

-

Automate reconciliation nightly; investigate mismatches immediately.

-

Place QR at eye level and ensure good lighting for faster scans.

-

Enable e-invoice in high-receipt categories.

-

Train staff: how to refund, how to check transaction history, how to respond to “no beep” cases.

-

Update KYC promptly when your store moves or changes ownership.

Buyer Tips (Practical)

-

Verify merchant name on the confirm screen before you pay.

-

Keep biometrics enabled; set a sensible wallet limit.

-

Use transaction history to track expenses and request refunds.

-

If a merchant’s code looks tampered, ask to scan at the counter/terminal instead of a loose sticker.

FAQ

Q1: What is an Alipay QR code?

A machine-readable square encoding a payment payload. It identifies the merchant or the buyer (in CPQR), optionally the amount, and security tokens/signatures.

Q2: Static vs dynamic —what’s the difference?

Static is fixed and cheap; buyer enters amount. Dynamic is generated per transaction, often includes the exact amount + nonce, reducing errors and fraud.

Q3: Is Alipay QR secure?

Yes—biometric/PIN auth, tokenization, rotating customer codes, risk engines, and KYC’d merchants deliver high trust.

Q4: How fast does settlement happen?

Commonly T+1 to the merchant’s bank; some categories support T+0 (same-day) with adjusted fees.

Q5: Can I refund a QR payment?

Yes, merchants can process full or partial refunds via their portal/app; buyers see the credit in their wallet promptly.

Q6: Does Alipay work overseas?

At many tourist-heavy stores and airports; scan works the same, with FX handled by Alipay or partners.

Conclusion

The genius of Alipay QR Codes payments is not the square itself but the orchestration around it. A century of banking risk practice collapses into a two-second decision; a merchant’s cashflow improves with T+1 settlement; and a buyer’s daily life becomes effortless through biometrics and one scan. QR won because it matched China’s reality—millions of small merchants, mobile-first consumers, thin margins, and a national push for inclusion.

As standards tighten and the Digital Yuan matures, the black-and-white square will keep doing its humble job, while the payload evolves: more tokenization, richer mini-program hooks, and deeper compliance. For students of payments and for practical operators alike, the lesson is clear: simplicity at the edge, sophistication at the core—that is the Alipay QR code in a line