Apps, Not Banks, Write the Future

“The future of money in China is not written by banks, but by apps.” – Fintech Scholar

In China, two platforms dominate the digital financial ecosystem: Alipay, created by Alibaba, and WeChat Pay, embedded within Tencent’s social messaging giant WeChat. Together, they control over 90% of China’s mobile payments market, redefining commerce, finance, and daily life.

This article compares Alipay vs WeChat Pay across their origins, ecosystems, strengths, weaknesses, cultural anchors, and global strategies. While both pursue similar goals, their design, philosophy, and execution diverge in fascinating ways.

Origins and Foundational Differences

Alipay

-

Launched: 2004 as an escrow service for Alibaba’s Taobao.

-

DNA: E-commerce trust → expanded to finance (Yu’e Bao, credit, insurance).

-

Built to solve China’s trust deficit in online shopping.

WeChat Pay

-

Launched: 2013, almost a decade later.

-

DNA: Social + lifestyle, embedded in WeChat messenger.

-

Started with peer-to-peer transfers and “red packets.”

-

Alipay’s DNA: Commerce + Finance

-

WeChat Pay’s DNA: Social + Daily Life

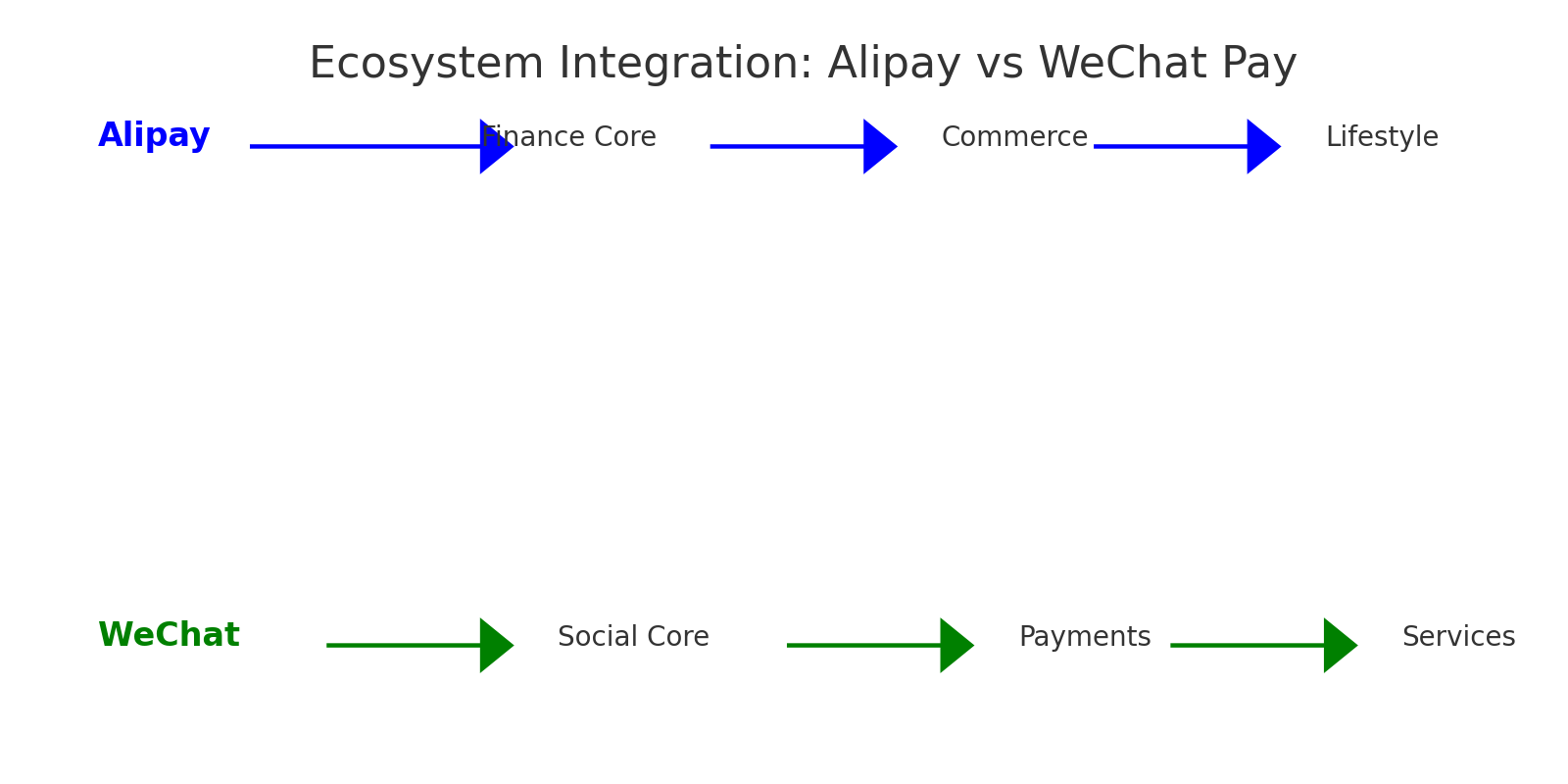

Ecosystem Integration

Alipay: Finance Super App

-

Part of Ant Group, operates like a digital bank.

-

Focus: Investments, loans, insurance, big payments.

-

Finance-first, commerce as secondary.

WeChat Pay: Lifestyle Super App

-

Works as a digital operating system with mini-programs.

-

Focus: Transport, food, gaming, social interactions.

-

Lifestyle-first, finance as add-on.

-

Alipay: Finance Core → Commerce → Lifestyle Add-ons

-

WeChat: Social Core → Payments → Services Expansion

User Experience and Core Strengths

Alipay

-

Preferred for big-ticket transactions.

-

Trusted for investments and financial services.

-

Professional, finance-oriented UX.

WeChat Pay

-

Dominant in daily transactions (food, taxis, red packets).

-

Seamlessly integrates into social interactions.

-

Fun, lifestyle-driven UX.

📊 Graph Suggestion: Market share trends:

-

2015 → Alipay 70%, WeChat 20%

-

2020 → Alipay 55%, WeChat 38%

-

2023 → Near equilibrium

Cultural Anchors

Alipay: Trust

-

Built around solving trust deficit in online shopping.

-

Reputation: secure, professional, finance-first.

WeChat: Culture

-

Red Packets (hongbao) turned tradition into tech.

-

Reputation: fun, social, culture-first.

Quote: “Alipay digitized commerce, WeChat digitized culture.” – Tech Journalist

Services Comparison

| Service Area | Alipay Strength | WeChat Strength |

|---|---|---|

| Payments | Secure, large transactions | Social, peer-to-peer |

| Investments | Yu’e Bao, funds | Limited |

| Credit | Huabei, Jiebei | WeBank integration |

| Insurance | Ant Insurance | Basic |

| Lifestyle | Add-ons | Deep integration |

| Global Reach | 50+ countries | 60+ countries |

Economic Impact

Alipay

-

Empowered SMEs with escrow + QR.

-

Built largest money market fund (Yu’e Bao).

-

Boosted SMEs via mini-programs.

-

Drove social commerce boom.

📌 Fact Box:

By 2020, 30M+ merchants accepted both Alipay and WeChat.

Criticisms and Risks

Alipay

-

Regulatory clampdowns on Ant IPO (2020).

-

Youth debt risks (Huabei/Jiebei).

-

Overexposure to finance.

-

Surveillance & censorship concerns.

-

Monopoly in lifestyle services.

-

Bans in India, scrutiny in U.S./E.U.

Quote: “WeChat is convenience with control; Alipay is finance with regulation.” – Policy Expert

Case Studies

Case 1: Singles’ Day (Alibaba 11/11 Festival)

-

Alipay processed trillions in sales in 24 hours.

Case 2: Lunar New Year Red Packets

-

WeChat Pay drove adoption to 800M+ users in weeks.

Global Ambitions

Alipay

-

Partners with local wallets (Paytm, GCash).

-

Focus: Chinese tourists + commerce abroad.

WeChat Pay

-

Partnered with Visa/MasterCard.

-

Focus: overseas consumption, travel.

| Feature | Alipay | WeChat Pay |

|---|---|---|

| Local Wallets | Strong | Weak |

| Tourist Focus | High | High |

| Global Brand | Finance-driven | Social-driven |

Evaluative Summary

Similarities

-

Both drive China’s cashless revolution.

-

Both rely on QR code payments.

-

Both integrate with Digital Yuan (CBDC).

Differences

-

Alipay: Finance-first, commerce roots.

-

WeChat Pay: Social-first, culture roots.

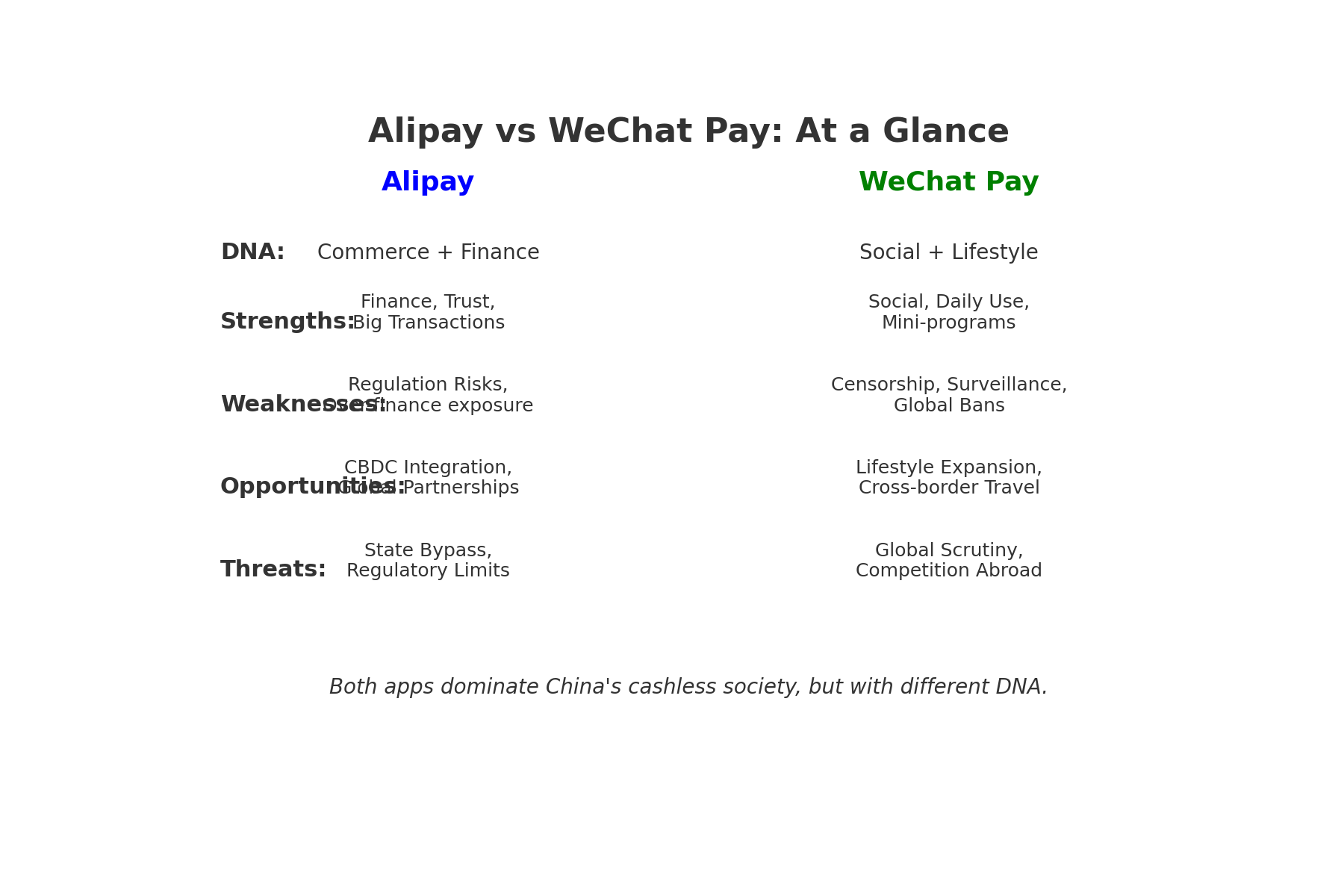

SWOT Comparison

| Factor | Alipay | WeChat Pay |

|---|---|---|

| Strength | Finance, trust | Social, daily use |

| Weakness | Regulation risks | Surveillance |

| Opportunity | CBDC integration | Lifestyle expansion |

| Threat | State bypass | Global scrutiny |

FAQs

Q1: Is Alipay bigger than WeChat Pay?

Alipay leads in finance and investments, while WeChat dominates daily lifestyle payments. Market share is now near equal.

Q2: Which is safer—Alipay or WeChat Pay?

Both use encryption and fraud checks. Alipay leans on finance trust, while WeChat focuses on secure peer-to-peer.

Q3: Can foreigners use Alipay and WeChat Pay?

Yes. Both apps now allow international cards to be linked.

Q4: Why did QR codes win in China?

Low infrastructure costs, easy adoption by SMEs, and universal smartphone penetration.

Q5: Do Alipay and WeChat support the Digital Yuan?

Yes, both act as distribution partners for China’s CBDC.

Q6: Will either expand globally?

Growth is strong in Asia, but both face scrutiny in Western markets.

Conclusion

Alipay and WeChat Pay are not just apps—they are digital titans that reshaped the Chinese economy.

-

Alipay: finance-first, trusted backbone of commerce.

-

WeChat Pay: social-first, embedded into culture and lifestyle.

Together, they created the world’s largest cashless society. While regulation, privacy, and geopolitics will test them, their dominance in China is unrivaled.

“Alipay and WeChat are not competitors alone; they are the dual architects of China’s digital future.” – Fintech Commentator