Future of Alipay and WeChat in China’s Digital Payments

China is already the world leader in mobile payments, and at the heart of this revolution stand two apps: Alipay and WeChat Pay. Together, they control over 90% of the mobile payments market and are used by more than 1 billion people daily. From buying coffee to investing in wealth products, Chinese citizens rely on these platforms more than cash or credit cards.

But what does the future of Alipay and WeChat in China’s digital payments look like? With the Digital Yuan, stricter government regulation, and global political challenges, their path forward is complex. This article explores their journey using a cause-effect lens while evaluating strengths, weaknesses, and future scenarios.

Introduction: Why China Leads the World in Digital Payments

China didn’t just adopt digital payments—it leapfrogged the world. While countries like the U.S. relied on credit cards for decades, China transitioned directly from cash to mobile payments. Today, a street vendor in Beijing or a luxury store in Shanghai will both prefer a QR code scan over paper money.

By 2022, more than 85% of urban transactions were conducted through Alipay or WeChat Pay.

Evolution of Mobile Payments in China

From Cash to QR Codes

The turning point came when QR codes became ubiquitous, low-cost, and simple. Unlike NFC or POS terminals, QR codes required no expensive infrastructure, making them attractive for merchants.

Why Credit Cards Never Took Off

China’s banking sector did not build the same credit card ecosystem as the U.S. Instead, mobile payments filled the gap.

Quote: “China skipped the credit card era and went straight into the mobile payment era.” – Fintech Analyst

Alipay: Finance-First Giant

Core Services: Payments, Loans, and Investments

Launched by Alibaba, Alipay was designed to build trust in e-commerce transactions. Over time, it expanded into:

-

Microloans (Huabei, Jiebei)

-

Wealth management (Yu’e Bao)

-

Insurance and financial products

Role in E-commerce and Alibaba Ecosystem

Alipay became the backbone of Alibaba’s retail empire, powering Singles’ Day, the world’s biggest shopping event.

WeChat Pay: Social-First Ecosystem

Integration with Messaging and Lifestyle

WeChat Pay grew from within WeChat, China’s “super app.” Instead of starting with finance, it started with social interaction, allowing users to transfer money as easily as sending a text.

The Red Packet Revolution

During Lunar New Year, WeChat Pay’s digital red packets (hongbao) became a cultural phenomenon, boosting adoption at lightning speed.

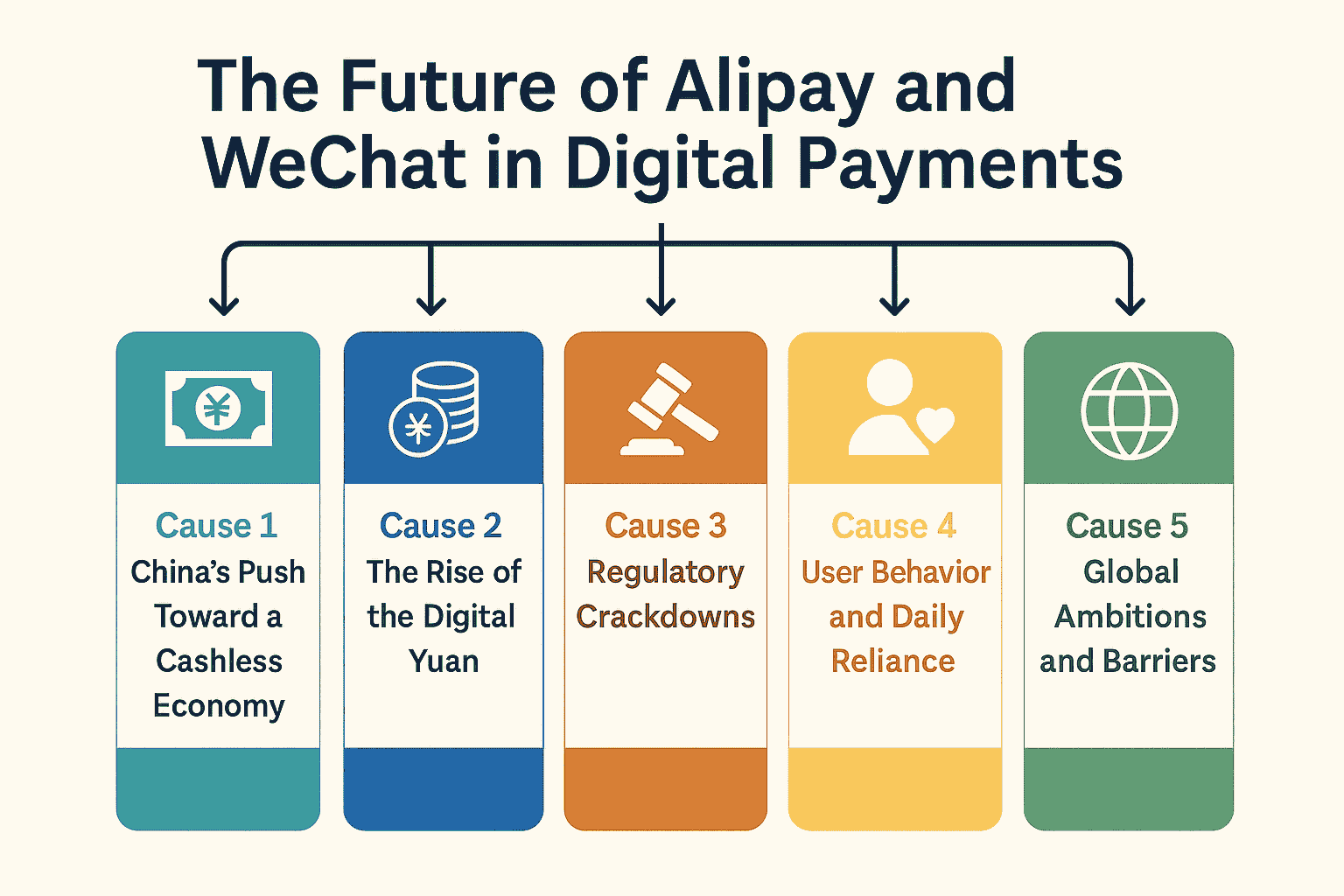

Cause 1: China’s Push Toward a Cashless Society

QR Code Payments as the Norm

In China, QR codes are everywhere—from luxury malls to street food vendors. This low-cost, scalable solution helped Alipay and WeChat gain dominance quickly. Unlike NFC-based systems such as Apple Pay, QR codes don’t need expensive terminals, which made adoption nearly universal.

Urban vs Rural Adoption

Urban areas transitioned rapidly, while rural areas lagged slightly due to internet access gaps. Still, by 2021, even farmers’ markets accepted mobile payments.

Fact Box: By 2020, 83% of retail transactions in China were conducted via mobile QR payments.

Effect

Both apps became daily essentials. Not carrying cash is normal for younger generations, and even older citizens are now adapting.

Future Outlook

The government’s cashless vision ensures Alipay and WeChat remain integral. However, their role may shift as Digital Yuan integration grows.

Cause 2: Rise of the Digital Yuan (CBDC)

How the Digital Yuan Works

The Digital Currency Electronic Payment (DCEP), or Digital Yuan, is China’s central bank digital currency (CBDC). Unlike Alipay and WeChat balances, which are tied to bank deposits, the Digital Yuan is directly issued by the People’s Bank of China (PBOC).

Alipay and WeChat as Distribution Partners

Instead of replacing them, the PBOC allowed both apps to distribute the Digital Yuan. Users can now access Digital Yuan wallets inside Alipay and WeChat.

Long-Term Impact on Market Power

In the short term, this strengthens the duopoly. But over time, as the state promotes its CBDC, the independence of Alipay and WeChat may shrink.

Quote: “The Digital Yuan is not meant to kill Alipay and WeChat—it is meant to tame them.” – Policy Analyst

Cause 3: Regulatory Oversight and Crackdowns

China’s government ensures fintech innovation aligns with national priorities. The last few years brought heavy regulation:

| Year | Regulation | Impact |

|---|---|---|

| 2010 | Payment licenses introduced | Legalized Alipay |

| 2020 | Ant Group IPO suspended | Limited lending & fintech services |

| 2021 | Antitrust laws expanded | Tencent investigated |

| 2022 | Data privacy laws enforced | Limited data monetization |

Ant Group IPO Suspension

The suspension of Ant Group’s record-breaking IPO signaled that unchecked fintech expansion was over.

Tencent Under Antitrust Probe

Tencent’s ecosystem dominance led regulators to scrutinize WeChat Pay’s mini-programs and market power.

Data Privacy and User Protection Laws

New privacy laws forced both platforms to limit data collection, cutting into advertising and profiling revenues.

Effect

Innovation is now policy-driven, not just user-driven.

Cause 4: User Behavior and Daily Reliance

When People Use Alipay vs WeChat Pay

-

Alipay: high-value purchases, investments, e-commerce.

-

WeChat Pay: small purchases, peer-to-peer transfers, social red packets.

-

Big purchases → Alipay dominance

-

Small/social purchases → WeChat Pay dominance

Generational Shifts and Expectations

-

Millennials & Gen Z expect seamless international use.

-

They also demand greater transparency in loans and fees.

-

Crypto-savvy users may seek integration with blockchain-based finance.

Effect

Alipay and WeChat remain daily essentials, but they must adapt to evolving user expectations.

Cause 5: Global Expansion and Barriers

Expansion in Asia and Belt & Road Countries

Alipay partnered with Paytm (India), GCash (Philippines), TrueMoney (Thailand), while WeChat Pay linked with Visa/MasterCard for overseas transactions.

By 2022, both apps were accepted in 60+ countries, mostly serving Chinese tourists.

Struggles in the West (US, EU, India)

-

India banned both apps due to political tensions.

-

The U.S. and EU scrutinize them for data security concerns.

Future Outlook

They will likely remain regional leaders in Asia and Africa, but face limits in Western markets.

SWOT Analysis of Alipay vs WeChat Pay

| Factor | Alipay | WeChat Pay |

|---|---|---|

| Strengths | Strong in finance, e-commerce integration | Strong in social payments & mini-programs |

| Weaknesses | Reliance on lending, regulatory clampdowns | Surveillance concerns, limited outside China |

| Opportunities | Digital Yuan integration, wealth products | Cross-border payments, social commerce |

| Threats | State bypass, competition from CBDC | Geopolitical bans, antitrust scrutiny |

Case Studies of Market Dominance

Case 1: Singles’ Day with Alipay

During Alibaba’s 11/11 shopping festival, Alipay processed trillions of yuan in transactions in just 24 hours.

Case 2: Lunar New Year with WeChat Red Packets

WeChat gamified red packets (hongbao), turning cultural traditions into viral digital adoption events.

Quote: “Alipay won commerce, WeChat won culture.” – Fintech Journalist

Future Scenarios for 2030

Scenario 1: Continued Duopoly

Alipay and WeChat adapt to regulation and maintain 90%+ dominance.

Scenario 2: Digital Yuan Reduces Their Power

The state app becomes central, and Alipay/WeChat become secondary channels.

Scenario 3: Global Integration

They expand into Asia, Africa, and Belt & Road nations, but remain limited in the West.

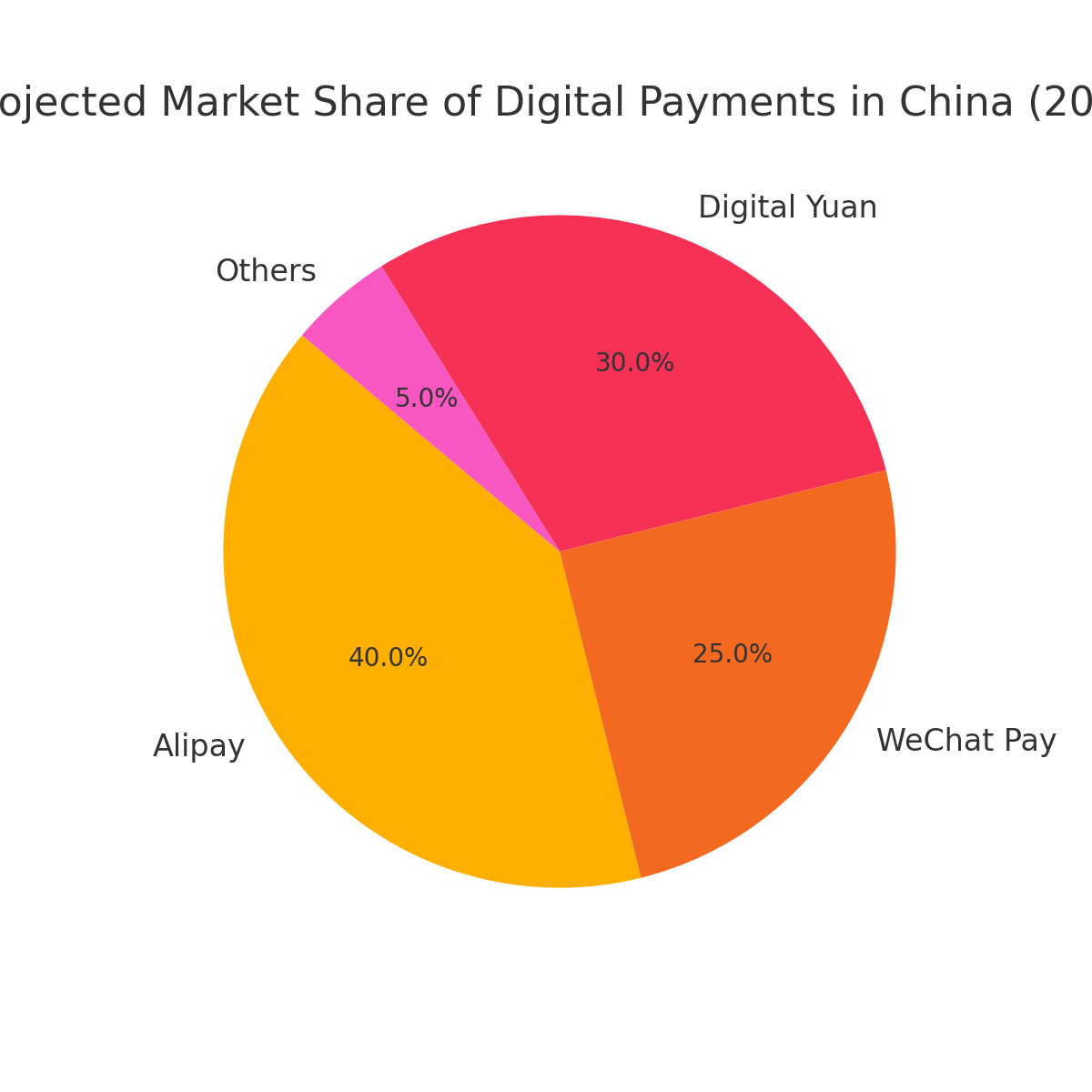

-

Digital Yuan: 30%

-

Alipay: 40%

-

WeChat Pay: 25%

-

Others: 5%

FAQs: Future of Alipay and WeChat in China’s Digital Payments

Q1. Will the Digital Yuan replace Alipay and WeChat?

No. It will integrate with them, but the apps will remain as front-end payment tools.

Q2. Which is better: Alipay or WeChat Pay?

Alipay is better for finance & big purchases, while WeChat Pay is better for social & daily payments.

Q3. Can foreigners use Alipay and WeChat Pay in China?

Yes, both apps now allow international credit cards to be linked.

Q4. Are Alipay and WeChat Pay expanding globally?

Yes, but mainly in Asia and tourist-heavy regions. Expansion in the West faces challenges.

Q5. Why did China skip credit cards?

Weak banking infrastructure and the rise of mobile-first ecosystems led China to jump straight to digital payments.

Q6. What is the biggest threat to Alipay and WeChat?

The Digital Yuan and geopolitical barriers remain their largest risks.

Conclusion: Digital Sovereignty and Coexistence

The future of Alipay and WeChat in China’s digital payments is not about rivalry between the two giants. Instead, it’s about coexistence with the Digital Yuan under the framework of China’s digital sovereignty.

-

Alipay will continue to dominate finance, investments, and commerce.

-

WeChat Pay will remain the leader in lifestyle, culture, and social transactions.

-

The Digital Yuan will act as the state-controlled backbone of this ecosystem.

By 2030, China’s digital payments market may surpass $80 trillion, and while regulation and politics will shape the landscape, Alipay and WeChat remain critical pillars of China’s digital economy.

Quote: “The future of Alipay and WeChat is not about rivalry; it is about survival within China’s vision of digital sovereignty.” – Tech Policy Expert