Introduction : WeChat and the Cashless Society in China

“In China today, cash is no longer king—WeChat is.” – Financial Times (2019)

China has rapidly evolved from a cash-dominated society into the most advanced cashless economy in the world. Unlike many countries where the transition to digital finance was driven by credit cards and banking institutions, China leapfrogged directly into mobile-first payments. At the heart of this financial revolution lies WeChat Pay, a platform that has reshaped how people spend, save, and share money.

This essay examines WeChat’s role in building a cashless society by analyzing the key problems China faced, the solutions WeChat introduced, the transformative social and economic impacts, and the challenges that still persist.

Issue 1: Inefficiency of Cash Transactions

Problem

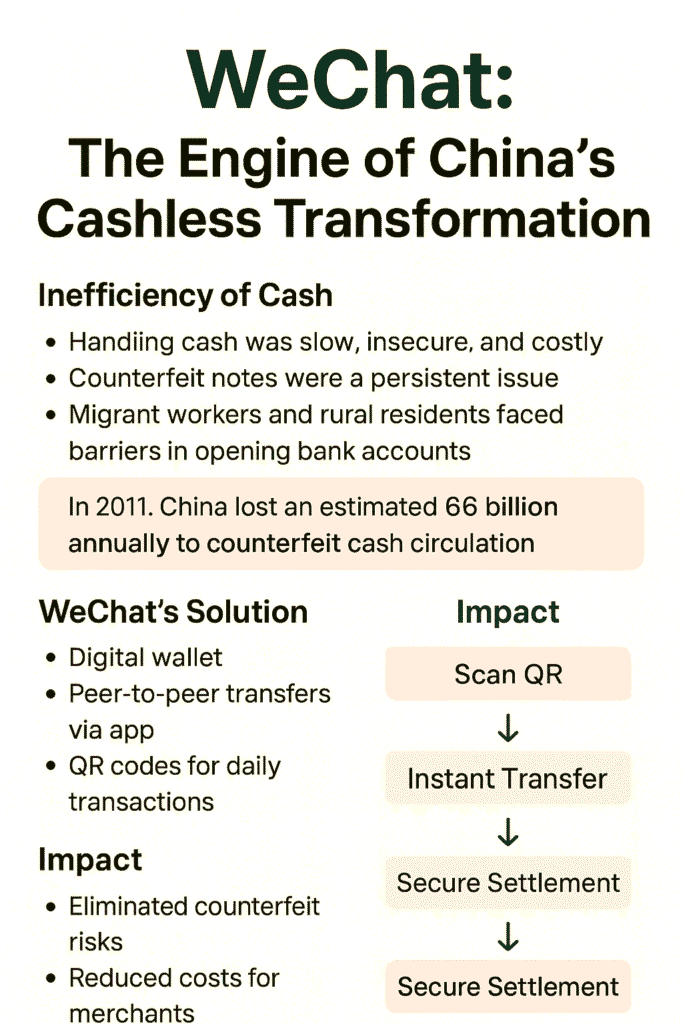

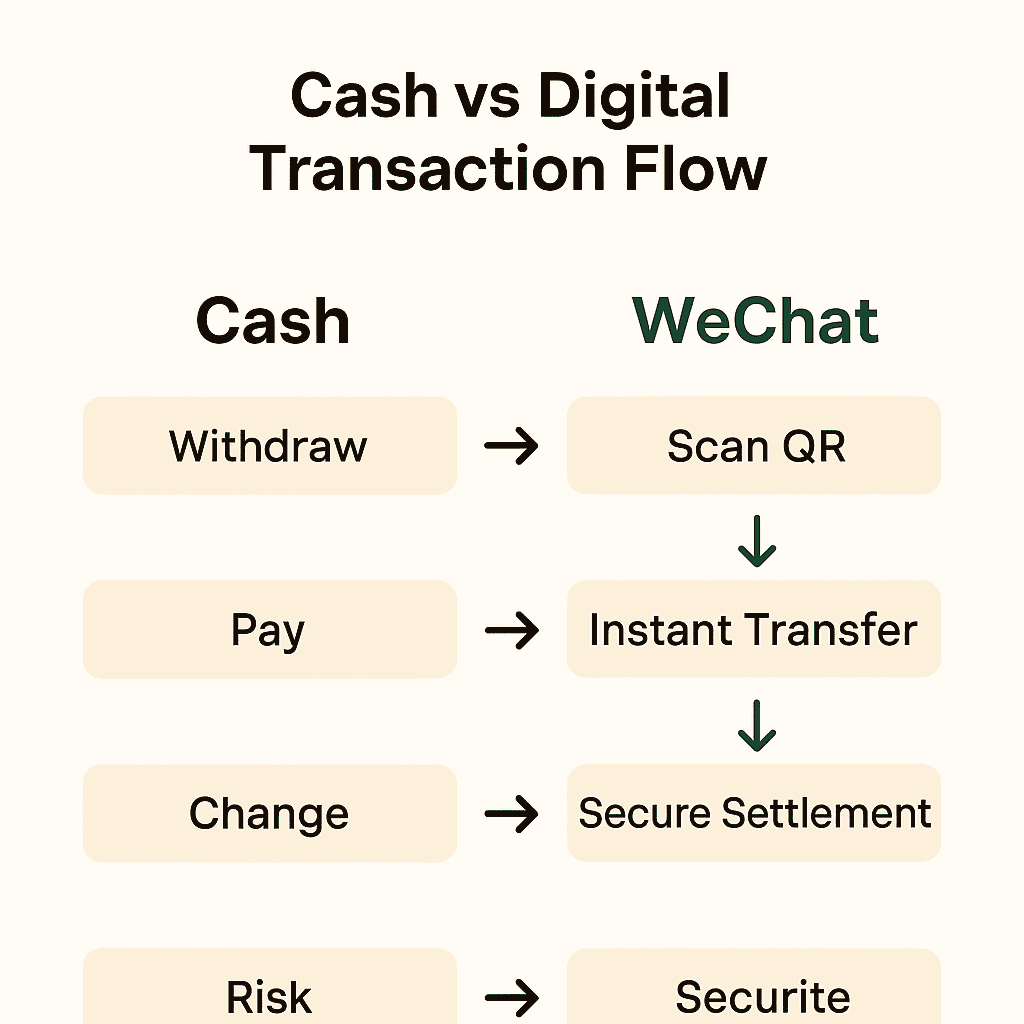

China’s reliance on physical cash was costly and insecure. Counterfeit notes circulated widely, transaction processes were slow, and many migrant workers and rural citizens lacked bank accounts.

-

Fact Box: In 2011, counterfeit money caused losses of more than $6 billion annually.

WeChat’s Solution: Digital Wallet

WeChat Pay introduced a secure, fast, and easy-to-use digital wallet. With peer-to-peer transfers, QR code payments, and no need for physical POS machines, it eliminated many of the risks and inefficiencies tied to cash.

Flow of Transactions:

Impact

By making payments faster and safer, WeChat Pay eliminated counterfeit risks, reduced merchant costs, and accelerated nationwide adoption of digital transactions.

Issue 2: Lack of Credit Card Infrastructure

Problem

China had very low credit card penetration—less than 20% of adults had access. Traditional POS terminals were expensive and excluded smaller merchants from digital payment systems.

WeChat’s Solution: QR Code Payments

WeChat enabled small businesses to accept payments simply by displaying a printed QR code. Merchants no longer needed costly infrastructure, which democratized access to digital finance.

Graph – Growth of WeChat QR Payments (2013–2020):

-

2013: negligible adoption

-

2016: 35% adoption

-

2020: 83% adoption

Impact

Every phone became a wallet, and every shop became a bank. This gave both wealthy urban consumers and small-town businesses equal access to the digital economy.

Issue 3: Cultural Shift in Payments

Problem

China’s payment culture was deeply tied to cash, especially in gifting traditions like hongbao (red envelopes). Meanwhile, younger generations leaned toward digital lifestyles.

WeChat’s Solution: Digital Red Packets

Launched during Lunar New Year in 2014, WeChat’s digital red envelopes went viral, gamifying traditional gifting and embedding digital transactions in cultural celebrations.

-

Fact Box: In 2019, over 823 million people used WeChat to send red envelopes during Lunar New Year.

Impact

This innovation normalized digital payments and accelerated adoption far beyond tech-savvy urban users, reaching small towns and rural areas.

Issue 4: Need for Financial Inclusion

Problem

Millions of Chinese citizens were excluded from formal banking. Traditional financial institutions catered mainly to urban elites.

WeChat’s Solution: Financial Access for All

WeChat wallets required only simple ID verification, making them accessible to almost anyone. With the help of WeBank, Tencent’s digital bank, WeChat also introduced microloans and small credit lines.

Table: Growth of Digital Financial Inclusion

| Year | % Adults with Digital Wallet Access |

|---|---|

| 2011 | 20% |

| 2016 | 65% |

| 2020 | 85% |

Impact

WeChat enabled migrant workers, farmers, and the rural poor to participate in the financial system, marking a significant milestone in economic inclusion.

Issue 5: Fragmented Daily Services

Problem

Paying bills, booking transport, and accessing healthcare all required separate processes, often involving cash.

WeChat’s Solution: The Super App

WeChat integrated multiple services—utilities, transport, food delivery, shopping, healthcare, and public services—into one platform.

Impact

With everything linked to WeChat Pay, the app became indispensable. Today, the average Chinese user spends over 4 hours per day inside WeChat.

Broader Social and Economic Impact

Social Impact

-

Changed lifestyle habits—people no longer carry cash.

-

Promoted peer-to-peer financial interactions, such as gifting and transfers.

-

Enhanced convenience and personal safety.

Economic Impact

-

Increased SME participation in digital markets.

-

Boosted consumer spending across industries.

-

Strengthened China’s domestic digital economy.

Mobile Payment Growth in China (2012–2020):

-

2012: $1 trillion

-

2015: $8 trillion

-

2020: $40 trillion+

Criticisms and Challenges

-

Privacy Concerns – WeChat collects vast amounts of user data, raising fears of state surveillance.

-

Monopoly Risks – WeChat and Alipay together control more than 90% of China’s payment market.

-

Exclusion of Elderly Citizens – Older populations struggle with digital adoption.

-

“Cashless convenience risks leaving behind those who are not digital natives.” – Social Policy Scholar

-

-

Regulatory Oversight – The Chinese government has increased scrutiny, promoting the Digital Yuan as a state-backed alternative.

Evaluative Analysis

| Issue | WeChat’s Role | Impact |

|---|---|---|

| Cash inefficiency | Digital wallet | Faster, safer transactions |

| Low credit card access | QR code adoption | SMEs empowered |

| Cultural red packets | Digital hongbao | Viral adoption |

| Financial exclusion | Wallet + WeBank | Inclusion for rural citizens |

| Fragmented services | Super app integration | Everyday reliance on WeChat |

Future of WeChat in China’s Cashless Economy

-

Integration with the Digital Yuan (CBDC)

-

AI-driven fraud detection and advanced security features

-

Blockchain settlements for transparency and efficiency

-

Global expansion, targeting international trade and tourism

-

Fact Box: By 2030, China aims for 95%+ digital payment penetration.

Conclusion

WeChat has been the single most influential driver of China’s transition to a cashless society. By tackling inefficiencies in cash transactions, addressing low credit card use, embracing cultural traditions, and promoting financial inclusion, it has redefined how people interact with money.

However, WeChat’s role in building a cashless society also brings challenges—privacy concerns, monopolistic risks, and regulatory oversight cannot be ignored. The future depends on balancing innovation with fairness, accessibility, and protection of individual freedoms.

“In China, cash is no longer king; WeChat is the emperor of payments.” – Tech Journalist

WeChat stands as both a global model for digital innovation and a warning about the concentration of power in financial ecosystems.

Frequently Asked Questions (FAQs)

1. What is WeChat’s role in building a cashless society?

WeChat simplified payments through QR codes, digital wallets, and super app integration, making digital finance accessible to nearly all citizens.

2. Why did China skip credit cards and move directly to mobile payments?

Low credit card penetration and high POS costs made credit-based payments impractical. Mobile QR codes provided an easier, cheaper alternative.

3. How has WeChat improved financial inclusion?

By requiring only basic ID verification, WeChat gave access to migrant workers, rural residents, and the unbanked, expanding participation in the economy.

4. What cultural role did WeChat red packets play?

Digital hongbao integrated cultural traditions with technology, making mobile payments socially engaging and widely accepted.

5. What are the risks of a WeChat-dominated payment system?

The main risks are privacy concerns, potential monopolistic dominance, exclusion of elderly users, and heavy government regulation.

6. What is the future of WeChat Pay?

It will likely integrate with the Digital Yuan, expand globally, and adopt blockchain and AI-driven security to remain a leader in digital finance.