In February 2023, a Shanghai visitor from Germany stood at a high-speed rail ticket counter clutching his Visa card — only to be told, politely but firmly, that the machine no longer accepted foreign cards. His Alipay International wallet had no balance. The queue behind him grew. A moment of helplessness in the world’s most cashless economy. Today, that scenario has a new solution: China’s official Digital Yuan, and crucially, foreigners can now access it. This guide explains everything you need to know.

1. What Is the Digital Yuan, and Why Does It Matter for Foreigners?

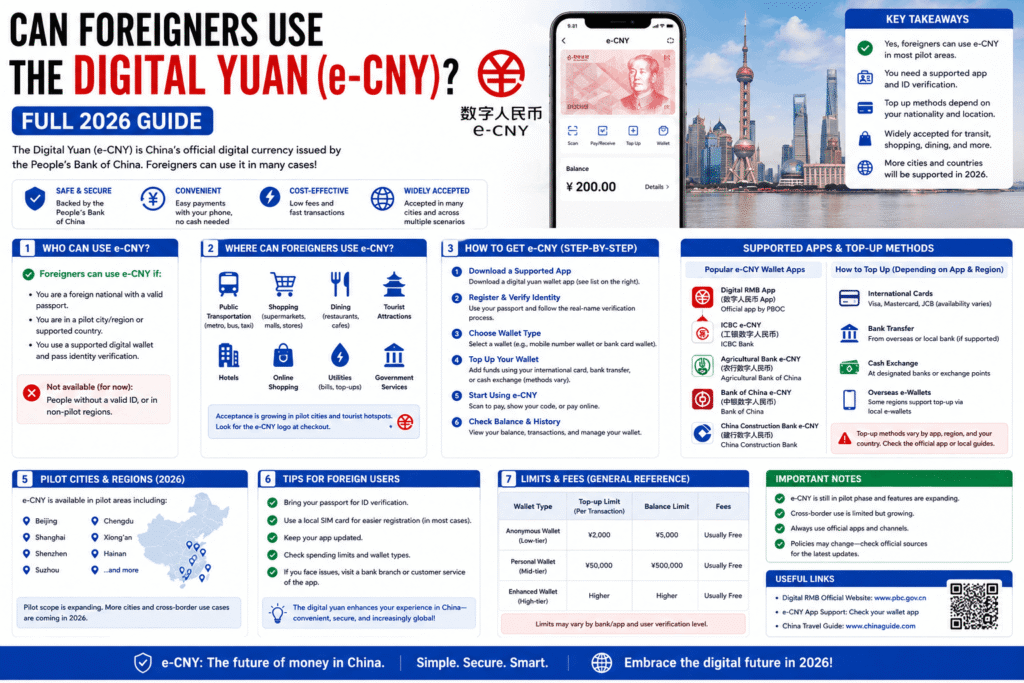

The Digital Yuan — officially the e-CNY — is China’s central bank digital currency (CBDC), issued and controlled by the People’s Bank of China (PBOC). Unlike Alipay or WeChat Pay, which are private platforms running on top of commercial bank infrastructure, the e-CNY is the money itself. It is a digital form of the renminbi, equivalent in value and legal status to physical cash.

For foreigners, the significance is profound. Until 2023, access to China’s mobile payment ecosystem required a Chinese bank account and a verified Chinese phone number — two things most tourists and short-term visitors simply cannot obtain. The e-CNY tourist wallet changes that calculation entirely, offering a pathway into cashless China that bypasses traditional banking requirements.

2. The Tourist Wallet: What It Allows (and What It Does Not)

The PBOC introduced the “tourist wallet” category specifically for inbound visitors. It operates on a tiered access model:

Tier 1 (Anonymous wallet, no ID required): You can hold up to ¥10,000 (~USD 1,380) and spend up to ¥50,000 per year. This is sufficient for most tourist trips. You register using only a foreign phone number.

Tier 2 (Verified wallet, passport required): Higher spending limits and the ability to receive transfers. You submit a passport scan through the app. Balance cap rises to ¥100,000.

What tourists cannot do: send money back abroad, transfer to non-Chinese accounts, or use e-CNY for international remittances. The system is explicitly designed for domestic consumption within China.

3. How to Register as a Foreigner: Step-by-Step

The process is more accessible than it appears. Here is the exact procedure as of 2026:

Step 1 — Download the e-CNY App. Search for “e-CNY” or “数字人民币” on the App Store or Google Play. The official app is published by “Digital Currency Institute, PBOC.” Ensure you are downloading the authentic version — there are clones.

Step 2 — Select your operator bank. Upon opening the app, choose a supported operator: Bank of China, ICBC, Agricultural Bank, China Construction Bank, or Postal Savings Bank. Bank of China is generally recommended for foreigners as it has the most robust international support.

Step 3 — Register with a foreign phone number. Unlike Alipay’s international version, the e-CNY app accepts foreign phone numbers directly. Enter your number, receive an SMS OTP, and complete basic registration. No Chinese phone number or SIM required.

Step 4 — Load funds using a foreign Visa or Mastercard. Navigate to “Top Up” and link your international card. The app supports Visa, Mastercard, American Express, and JCB. Your card is charged in your home currency; the app converts to CNY at the prevailing exchange rate with a small spread.

Step 5 — Spend. Use the QR code scan function — the same QR codes used by Alipay and WeChat Pay are often compatible, as major merchants increasingly support all three platforms. Alternatively, tap-to-pay via NFC where available.

4. Where Can Foreigners Spend e-CNY in China?

Acceptance has grown rapidly since pilot programs began in Shenzhen in 2020. By 2026, e-CNY is accepted at:

- All state-owned supermarkets (RT-Mart, Hema Fresh, CR Vanguard)

- Major restaurant chains (McDonald’s China, KFC, Starbucks, local franchises)

- Beijing, Shanghai, Guangzhou, Shenzhen, Chengdu subway systems

- Most hotels rated 3-star and above in Tier 1 and Tier 2 cities

- Major e-commerce platforms when accessed domestically

- Tourist attractions in pilot cities including the Forbidden City, West Lake, and Disneyland Shanghai

Coverage in rural areas and small independent shops remains patchy. Always carry some physical RMB cash as backup when venturing off the standard tourist circuit.

5. e-CNY vs Alipay International vs WeChat Pay for Foreigners: Comparison

| Feature | e-CNY Tourist Wallet | Alipay International | WeChat Pay (Foreign Card) |

|---|---|---|---|

| Requires Chinese bank account | No | No | No |

| Requires Chinese phone number | No | No | Recommended |

| Foreign card top-up | Yes (Visa/MC/Amex) | Yes (Visa/MC) | Yes (Visa/MC) |

| Annual spending limit (no ID) | ¥50,000 | ¥50,000 | ¥50,000 |

| Offline/NFC payments | Yes (hardware wallet option) | Limited | No |

| Government issued / CBDC | Yes | No | No |

| Acceptance in 2026 | Growing rapidly | Widest coverage | Widest coverage |

| Works without internet | Yes (hardware wallet) | No | No |

The e-CNY’s unique advantage is its offline capability via the hardware wallet (a physical card issued by operator banks). This matters in underground metros, mountainous tourist areas, and anywhere signal is unreliable.

6. Privacy Considerations: What the Chinese Government Can See

This question is asked by every foreign user, and it deserves a candid answer. The e-CNY is programmable money issued by a central authority. The PBOC has full visibility of all transactions at the systemic level. The government’s stated position is that individual transactions below a certain threshold are “anonymised” from commercial operators — but not from the PBOC itself.

For a tourist buying coffee and metro tickets, the practical privacy implications are negligible. For business travellers handling sensitive transactions, the calculus is different. The same surveillance concern applies, in varying degrees, to Alipay and WeChat Pay — both of which comply with Chinese law and respond to government data requests. The e-CNY is simply more explicit about its central visibility.

Travellers from Western nations should be aware that their government may have its own advisories regarding the use of Chinese digital payment platforms. Consult your foreign ministry’s travel guidance before departure.

7. The e-CNY Hardware Wallet: For Travellers Without Smartphones

An underappreciated innovation of the e-CNY system is the hardware wallet — a physical card that stores digital yuan and transacts via NFC, requiring no internet connection and no smartphone. These are available at Bank of China branches in major cities and at certain airports.

For elderly travellers, those with basic phones, or anyone visiting remote regions where network coverage is unreliable, the hardware wallet is a genuine breakthrough. Load it at an ATM or bank counter, and spend anywhere NFC terminals are present — which, in modern Chinese retail, is most places.

8. Practical Tips for Foreigners Using e-CNY

Download before you land. App Store availability varies by country. Download the e-CNY app at home while your VPN is not yet needed. Once in China, the Great Firewall may complicate Google Play access on Android.

Load in small amounts initially. Test a ¥500–1,000 top-up first to confirm your card works with the system before loading larger sums. Some foreign cards trigger fraud alerts for international CNY transactions.

Keep your phone charged. Like all mobile payments, the e-CNY app requires a functioning phone. Carry a power bank in major tourist areas where walking distances are long and charging opportunities scarce.

Note the exchange rate spread. The rate offered during card top-up is not always competitive. For large sums, consider topping up via a Bank of China ATM withdrawal (using your foreign debit card for RMB cash, then depositing to the digital wallet) or using a Wise card to minimise conversion costs.

Frequently Asked Questions

Q: Can I use e-CNY outside China?

A: No. The e-CNY is currently a domestic-only currency. Cross-border trials (the mBridge project) exist but are not yet available to individual consumers.

Q: What happens to unused e-CNY when I leave China?

A: You can request a refund back to your linked card through the app. The process typically takes 3–7 business days and applies the spot exchange rate at time of refund.

Q: Is e-CNY the same as cryptocurrency?

A: No. It shares the “digital” aspect with cryptocurrency but is entirely centralised, issued and controlled by the PBOC. It cannot be mined, has no blockchain in the Bitcoin sense, and carries no speculative value — it is simply digital cash.

Q: Do I need a VPN to use the e-CNY app?

A: No, and in fact using a VPN while operating e-CNY may violate China’s VPN regulations. The app functions normally on the Chinese domestic internet without any circumvention tools.

Q: Can I receive payments into my e-CNY tourist wallet?

A: Tier 2 verified wallets allow incoming transfers from other e-CNY users. Tier 1 anonymous wallets are spend-only. You cannot receive international wire transfers into an e-CNY wallet.

Conclusion: A New Era for Cashless Travel in China

The arrival of the e-CNY tourist wallet marks a meaningful turning point in China’s relationship with the outside world. For decades, the country’s payment infrastructure was effectively a walled garden — accessible only to those with Chinese bank accounts and domestic phone numbers. The Digital Yuan cracks that wall open, not wide, but enough for the determined traveller to step through.

For the German visitor at that Shanghai ticket counter in 2023, the solution now exists in his pocket. Download the app, link a Visa card, and the world’s most cashless society becomes, at last, navigable. That is the quiet but consequential promise of the Digital Yuan for foreigners in 2026.